The purpose of Veterans Affairs (VA) home loans is to provide a pathway to homeownership for those who have sacrificed so much by serving our nation. As the Veterans Administration says of the program:

“The objective of the VA Home Loan Guaranty program is to help eligible Veterans, active-duty personnel, surviving spouses, and members of the Reserves and National Guard purchase, retain, and adapt homes in recognition of their service. . . .”

For over 75 years, VA home loans have provided millions of veterans and their families the opportunity to purchase their own homes.

2020 Data on VA Home Loans

1,246,817 home loans are guaranteed by the Veterans Administration

The average VA loan amount totals $301,044

178,171 of those using a VA Loan are first-time homebuyers

As we reflect on their sacrifice and honor our nation’s veterans, it’s important to ensure all veterans know the full extent of benefits VA home loans offer. As Jeff London, Director of the VA Home Loan Program, says:

“VA loans offer an extraordinary opportunity for veterans because of lower interest rates, lower monthly payments, no or low-down payments, and no private mortgage insurance.”

Those who qualify for a VA home loan are eligible for the following:

Borrowers can often purchase a home with no down payment. In 2020, 350,094 individuals using a VA Loan were able to purchase their homes without putting money down.

Many other loans with down payments under 20% require Private Mortgage Insurance (PMI). VA Loans do not require PMI, which means veterans can save on their monthly housing costs.

Finally, VA-Backed Loans often offer the most competitive terms and interest rates.

Bottom Line

One way we can honor and thank our veterans this year is to ensure they have the best information about the benefits of VA home loans. Homeownership is the American Dream. Our veterans sacrifice so much in service to our nation and deserve to achieve their homeownership goals. Thank you for your service.

Applying for a mortgage is a big step towards homeownership, but it doesn’t need to be one you fear. Here are some tips to help you prepare.

Know your credit score and work to build strong credit. When you’re ready, lean on your agent to connect you with a lender so you can get pre-approved and begin your home search.

Any major life change can be scary, and buying a home is no different. Let’s connect so you have an advisor by your side to take the fear out of the equation.

Buyers in today’s market often have questions about the importance of getting a home appraisal and an inspection. That’s because high buyer demand and low housing supply are driving intense competition and leading some buyers to consider waiving those contingencies to stand out in the crowded market.

But is that the best move? Buying a home is one of the most important transactions in your lifetime, and it’s critical to keep your best interests in mind. Here’s a breakdown of what to expect from the appraisal and the inspection, and why each one can potentially save you a lot of time, money, and headaches down the road.

Home Appraisal

The home appraisal is a critical step for securing a mortgage on your home. As Home Light explains:

“. . . lenders typically require an appraisal to ensure that your loan-to-value ratio falls within their underwriting guidelines. Mortgages are secured loans where the lender uses your home as collateral in case you default on the agreed-upon payments.”

Put simply: when you apply for a mortgage, an unbiased appraisal – typically required by your lender – is the best way to verify the value of the home. That appraisal ensures the lender doesn’t loan you more than what the home is worth.

When buyers are competing like they are today, bidding wars and market conditions can push prices up. A buyer’s contract price may end up higher than the value of the home – this is known as an appraisal gap. In today’s market, it’s common for the seller to ask the buyer to make up the difference when an appraisal gap occurs. That means, as a buyer, you may need to be prepared to bring extra money to the table if you really want the home.

Home Inspection

Like the appraisal, the inspection is important because it gives an impartial evaluation of the home. While the appraisal determines the current value of the home, the inspection determines the current condition of the home. As the American Society of Home Inspectors puts it:

“Home inspections are the opportunity to discover major defects that were not apparent at a buyer’s showing. . . . Your home inspection is to help you make an informed decision about the house, including its condition.”

If there are any concerns during the inspection – an aging roof, a malfunctioning HVAC system, or any other questionable items – you have the option to discuss and negotiate any potential issues with the seller. Your real estate advisor can help you navigate this process and negotiate what, if any, repairs need to be made before the sale is finalized.

Keep in mind – home inspections are critical because they can shed light on challenges you may face as the new homeowner. Without an inspection, serious, sometimes costly issues could come as a surprise later on.

Bottom Line

Both the appraisal and the inspection are important steps in the homebuying process. They protect your best interests as a buyer by providing unbiased information about the home’s value and condition. Let’s connect so you have an expert guiding you throughout the entire process.

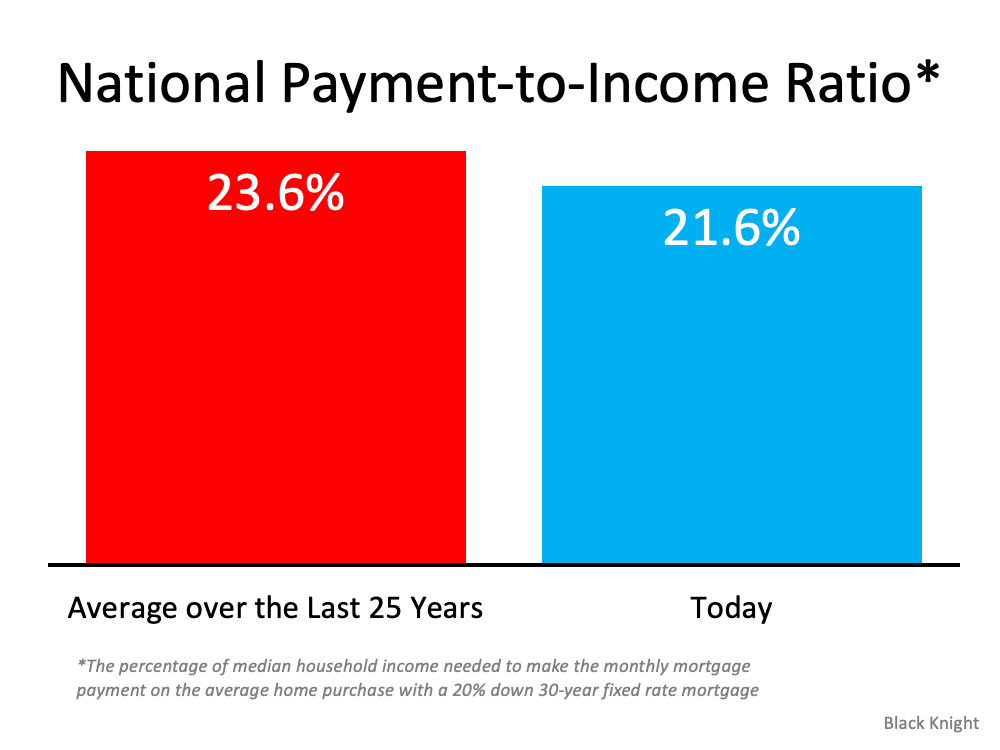

It’s impossible to research the subject of buying a home without coming across a headline declaring that the fall in home affordability is a crisis. However, when we add context to the most recent affordability statistics, we soon realize that, though homes are less affordable than they have been over the last few years, they are more affordable than they historically have been.

Black Knight, a premier provider of data and analytics for the mortgage industry, just released their latest Monthly Mortgage Monitor which includes a new analysis of the affordability situation. Here’s what the report reveals:

“The monthly payment required to purchase the average priced home with a 20% down 30-year fixed rate mortgage increased by nearly 20% (+$210) over the first nine months of 2021, . . . It now requires 21.6% of the median household income to make the monthly mortgage payment on the average home purchase, the least affordable housing has been since 30-year rates rose to nearly 5% back in late 2018.”

Basically, the report shows that homes are less affordable today than at any other time in the last three years. However, in a previous report earlier this year, Black Knight calculated that the percentage of the median household income to make the monthly mortgage payment on the average home purchase over the last 25 years was 23.6% (see graph below):Today’s payment-to-income ratio is more affordable than the average over the last 25 years. Given that context, we can see that American households still have the same ability to be homeowners as their parents did 20 years ago.

This confirms the recent analysis of ATTOM Data resources where Todd Teta, Chief Product and Technology Officer, explains:

“The typical median-priced home around the U.S. remains affordable to workers earning an average wage, despite prices that keep going through the roof. Super-low interests and rising pay continue to be the main reasons why.”

Bottom Line

It’s true that it’s less affordable to buy a home today than it has been the last few years. However, it’s more affordable to buy today than the average over the last 25 years. In other words, homes are less affordable, but they’re not unaffordable. That’s an important distinction.

If you’re looking to buy or sell a house, chances are you’ve heard talk about today’s rising home prices. And while this increase in home values is great news for sellers, you may be wondering what the future holds. Will prices continue to rise with time, or should you expect them to fall?

To answer that question, let’s first understand a few terms you may be hearing right now.

Appreciation is an increase in the value of an asset.

Depreciation is a decrease in the value of an asset.

Deceleration is when something happens at a slower pace.

It’s important to note home prices have increased, or appreciated, for 114 straight months. To find out if that trend may continue, look to the experts. Pulsenomics surveyed over 100 economists, investment strategists, and housing market analysts asking for their five-year projections. In terms of what lies ahead, experts say the market may see some slight deceleration, but not depreciation.

Here’s the forecast for the next few years:As the graph above shows, prices are expected to continue to rise, just not at the same pace we’ve seen over the last year. Over 100 experts agree, there is no expectation for price depreciation. As the arrows indicate, each number is an increase, which means prices will rise each year.

Bill McBride, author of the blog Calculated Risk, also expects deceleration, but not depreciation:

“My sense is the Case-Shiller National annual growth rate of 19.7% is probably close to a peak, and that year-over-year price increases will slow later this year.”

“. . . home price appreciation is on the cusp of flipping to a deceleratingtrend.”

A recent article from realtor.com indicates you should expect:

“. . . annual price increases will slow to a more normal level, . . .”

What Does This Deceleration Mean for You?

What experts are projecting for the years ahead is more in line with the historical norm for appreciation. According to data from Black Knight, the average annual appreciation from 1995-2020 is 4.1%. As you can see from the chart above, the expert forecasts are closer to that pace, which means you should see appreciation at a level that’s aligned with a more normal year.

If you’re a buyer, don’t expect a sudden or drastic drop in home prices – experts say it won’t happen. Instead, think about your homeownership goals and consider purchasing a home before prices rise further.

If you’re a seller, the continued home price appreciation is good news for the value of your house. Work with an agent to list your house for the right price based on market conditions.

Bottom Line

Experts expect price deceleration, not price depreciation over the coming years. Let’s connect to talk through what’s happening in the housing market today, where things are headed, and what it means for you.

Let me start by saying that I am excited for you. The only reason that you would be reading this is because you have determined that owning a home may be right for you. It means that you are at least exploring the possibilities and considering what life would look like as a homeowner. That alone is exciting and a proposition that is full of promise.

Your reading this also means that I have a chance to earn the opportunity to help you to achieve Your Own Personal American Dream. One of the reasons that I love my job is because I get to help people just like you create and shape their lifestyle through homeownership. It is truly an honor when someone allows me that opportunity. So let me share with you how I can help.

All of our services start with a quick 15 – 30 minute coaching call which is a basic introductory consultation. On that call you take out your dream paint brush and start painting a picture of what your American Dream looks like. I will ask you some specific questions about your plans and qualifications and, if we both decide at the end of that call that we should move to the next stage, we will schedule your comprehensive buyer consultation.

Depending on your experience as a homeowner/future homeowner, right off the bat you will notice that my approach is much different than 98% or more of real estate agents that you may have talked to or even worked with in the past. Since 1989 I have been a full time REALTOR® and have had the privilege of helping hundreds of families, couples, and individuals buy and sell homes. I discovered along the way that the more time taken in planning and preparing up front, the more successful the home purchase or sale would be in the end.

As your HousingCoach℠ I will help you to develop and solid home buying game plan which will incorporate your current circumstances and your plans, goals, and dreams for the next 5, 10, or even 20 or more years into the future. Your success as a home buyer can be measured in how well you are equipped and prepared to find the home that best fits your plan, compete against other home buyers, negotiate with the seller from a place of strength, and complete the transaction with as few hassles as possible.

Once we decide to work together I will help you to build out your Home Buying Game Plan, assemble your Home Buying Real Estate Team, structure and activate an automated Home Search Process, prepare you to have the best competitive advantage, negotiate on your behalf to get the best possible deal, and coordinate all of the transaction requirements and activities until the deal is closed.

My goal is that in the process of helping you to achieve Your Personal American Dream, that you are provided a personal level of service such that you feel compelled to refer me and my services to your family, friends, co-workers, and people you care about. That is how I will know I did my job well.

![The Mortgage Process Doesn’t Have To Be Scary [INFOGRAPHIC]](https://housingcoach.com/wp-content/uploads/2021/10/20211029-KCM-Share-549x300-1.png)

![The Mortgage Process Doesn’t Have To Be Scary [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/10/27142914/20211029-KCM-Share-549x300.png)

![The Mortgage Process Doesn’t Have To Be Scary [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/10/27141854/20211029-MEM.png)