When mortgage forbearance plans were first announced and the pandemic surged through the country in early 2020, many homeowners were allowed to pause their mortgage payments. Some analysts were concerned that once the forbearance program ended, the housing market would experience a wave of foreclosures like what happened after the housing bubble 15 years ago.

Here’s a look at why that isn’t the case.

1. There Are Fewer Homeowners in Trouble This Time

After the last housing crash, over nine million households lost their homes to a foreclosure, short sale, or because they gave it back to the bank. Many believed millions of homeowners would face the same fate again this time.

However, today’s data shows that most homeowners exited their forbearance plan either fully caught up on payments or with a plan from the bank that restructured their loan in a way that allowed them to start making payments again. The latest data from the Mortgage Bankers Association (MBA) studies how people exited the forbearance program from June 2020 to November 2021.

Here are those findings:

38.6% left the program paid in full

19.9% made their monthly payments during the forbearance period

16.8% left the program still in trouble and without a loss mitigation plan in place

2. Those Left in the Program Can Still Negotiate a Repayment Plan

As of last Friday, the total number of mortgages still in forbearance stood at 890,000. Those who remain in forbearance still have the chance to work out a suitable plan with the servicing company that represents their lender. And the servicing companies are under pressure to do just that by both federal and state agencies.

Rick Sharga, Executive Vice President at RealtyTrac, says in a recent tweet:

“The [Consumer Financial Protection Bureau] and state [Attorneys General] look like they’re adopting a ‘zero tolerance’ approach to mortgage servicing enforcement. Likely that this will limit #foreclosure activity for a good part of 2022, while servicers explore all possible loss [mitigation] options.”

For more information, read the warning issued by the Attorney General of New York State.

3. Most Homeowners Have More Than Enough Equity To Sell Their Homes

For those who can’t negotiate a solution and the 16.8% who left the forbearance program without a work-out, many will have enough equity to sell their homes and leave the closing with cash instead of facing foreclosures.

Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home. As Frank Martell, President & CEO of CoreLogic,explains:

“Not only have equity gains helped homeowners more seamlessly transition out of forbearance and avoid a distressed sale, but they’ve also enabled many to continue building their wealth.”

4. There Have Been Far Fewer Foreclosures Over the Last Two Years

One of the seldom-reported benefits of the forbearance program was that it allowed households experiencing financial difficulties prior to the pandemic to enter the program. It gave those homeowners an extra two years to get their finances in order and work out a plan with their lender. That prevented over 400,000 foreclosures that normally would have come to the market had the new forbearance program not been available. Otherwise, the real estate market would have had to absorb those foreclosures. Here’s a graph depicting this data:

5. The Current Market Can Easily Absorb Over a Million New Listings

When foreclosures hit the market in 2008, they added to the oversupply of houses that were already for sale. That resulted in over a nine-month supply of listings, and anything over a six-month supply can cause prices to depreciate.

It’s exactly the opposite today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) reveals:

“Total housing inventory at the end of November amounted to 1.11 million units, down 9.8% from October and down 13.3% from one year ago (1.28 million). Unsold inventory sits at a 2.1-month supply at the current sales pace, a decline from both the prior month and from one year ago.”

A balanced market would have approximately a six-month supply of inventory. At 2.1 months, the market is severely understocked. Even if one million homes enter the market, there still won’t be enough inventory to meet the current demand.

Bottom Line

The end of the forbearance plan will not cause any upheaval in the housing market. Sharga puts it best:

“The fact that foreclosure starts declined despite hundreds of thousands of borrowers exiting the CARES Act mortgage forbearance program over the last few months is very encouraging. It suggests that the ‘forbearance equals foreclosure’ narrative was incorrect. . . .”

There are a lot of questions right now regarding the real estate market as we head into 2022. The forbearance program is coming to an end and mortgage rates are beginning to rise.

With all of this uncertainty, anyone with a megaphone – from the mainstream media to a lone blogger – has realized that bad news sells. Unfortunately, we’ll continue to see a rash of troublesome headlines over the next few months. To make sure you aren’t paralyzed by a headline, turn to reliable resources for a look at what to expect from the housing market next year.

There are already alarmist headlines starting to appear. Here are two recent topics you may have seen in the news.

1. Foreclosures Are Spiking Today

There are a number of headlines circulating that call out the rising foreclosures in today’s real estate market. Those stories focus on an overly narrow view on that topic: the current volume of foreclosures compared to 2020. They emphasize that we’re seeing far more foreclosures this year compared to last.

That seems rather daunting. However, though it’s true foreclosures have been up over the 2020 numbers, it’s important to realize that there were virtually no foreclosures last year because of the forbearance plan. If we compare this September to September of 2019 (the last normal year), foreclosures were down 70% according to ATTOM.

Even Rick Sharga, an Executive Vice President of the firm that issued the report referenced in the above article, says:

“As expected, now that the moratorium has been over for three months, foreclosure activity continues to increase. But it’s increasing at a slower rate, and it appears that most of the activity is primarily on vacant and abandoned properties, or loans in foreclosure prior to the pandemic.”

Homeowners who have been impacted by the pandemic are not generally the ones being burdened right now. That’s because the forbearance program has worked. Ali Haralson, President of Auction.com, explains that the program has done a remarkable job:

“The tsunami of foreclosures many feared in the early days of the pandemic has not materialized thanks in large part to the swift and decisive foreclosure protections put in place by government policymakers and the mortgage servicing industry.”

And the government is still making sure homeowners have every opportunity to stay in their homes. Rohit Chopra, the Director of the Consumer Financial Protection Bureau (CFPB), issued this statement just last week:

“Failures by mortgage servicers and regulators worsened the impact of the economic crisis a decade ago. Regulators have learned their lesson, and we will be scrutinizing servicers to ensure they are doing all they can to help homeowners and follow the law.”

2. Rising Mortgage Rates Will Slow the Housing Market

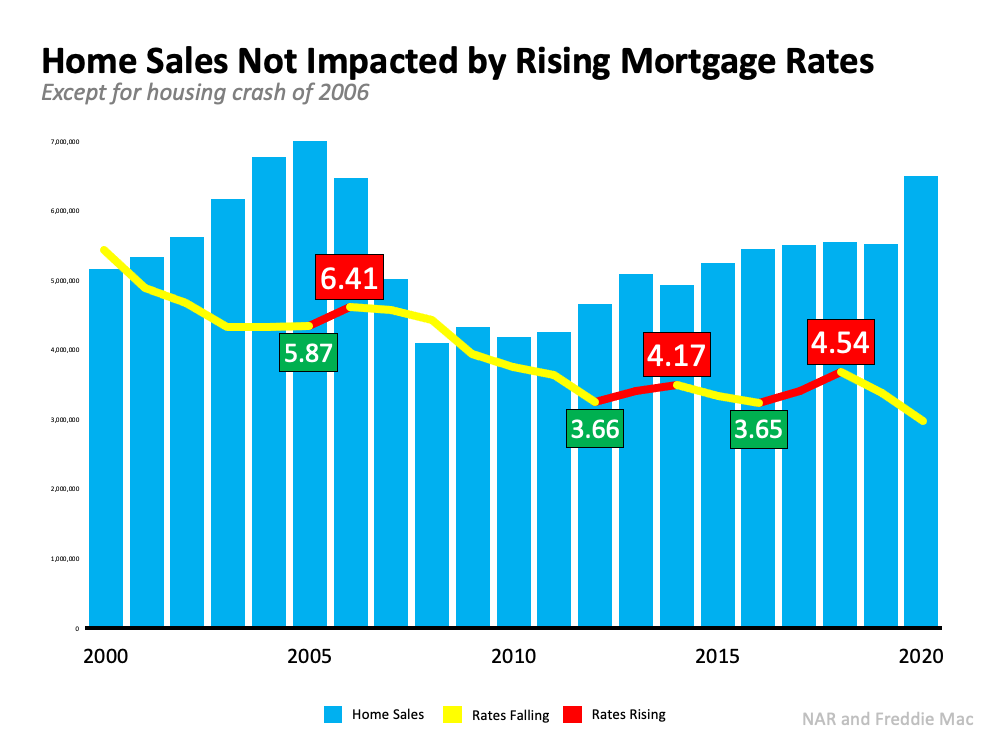

Another topic that’s generating frequent headlines is the rise in mortgage rates. Some people are expressing concern that rising rates will negatively impact the housing market by causing home sales to dramatically decline. The resulting headlines are raising unneeded alarm bells. To counteract those headlines, we need to take a look at what history tells us. Looking at data over the last 20 years, there’s no evidence that an increase in rates dramatically forces sales to come to a halt. Nor does home price appreciation come to a screeching stop. Let’s look at home sales first:The last three times rates increased (shown in the graph above in red), sales (depicted in blue in the graph) remained rather consistent. It’s true that sales fell rather dramatically from 2007 through 2010, but mortgage rates were also falling at the time. The next two instances showed no meaningful drop in sales.

Now, let’s take a look at home price appreciation (see graph below):Again, we see that a rise in rates didn’t cause prices to depreciate. Outside of the years following the crash, prices continued to appreciate, just at a slower rate.

Bottom Line

There’s a lot of misinformation out there. If you want the best advice on what’s happening in the current housing market, let’s connect.

With forbearance plans coming to an end, many are concerned the housing market will experience a wave of foreclosures similar to what happened after the housing bubble 15 years ago. Here are a few reasons why that won’t happen.

There are fewer homeowners in trouble this time

After the last housing crash, about 9.3 million households lost their homes to a foreclosure, short sale, or because they simply gave it back to the bank.

As stay-at-home orders were issued early last year, the fear was the pandemic would impact the housing industry in a similar way. Many projected up to 30% of all mortgage holders would enter the forbearance program. In reality, only 8.5% actually did, and that number is now down to 2.2%.

As of last Friday, the total number of mortgages still in forbearance stood at 1,221,000. That’s far fewer than the 9.3 million households that lost their homes just over a decade ago.

Most of the mortgages in forbearance have enough equity to sell their homes

Due to rapidly rising home prices over the last two years, of the 1.22 million homeowners currently in forbearance, 93% have at least 10% equity in their homes. This 10% equity is important because it enables homeowners to sell their homes and pay the related expenses instead of facing the hit on their credit that a foreclosure or short sale would create.

The remaining 7% might not have the option to sell, but if the entire 7% of those 1.22 million homes went into foreclosure, that would total about 85,400 mortgages. To give that number context, here are the annual foreclosure numbers for the three years leading up to the pandemic:

2017: 314,220

2018: 279,040

2019: 277,520

The probable number of foreclosures coming out of the forbearance program is nowhere near the number of foreclosures that impacted the housing crash 15 years ago. It’s actually less than one-third of any of the three years prior to the pandemic.

The current market can absorb listings coming to the market

When foreclosures hit the market back in 2008, there was an oversupply of houses for sale. It’s exactly the opposite today. In 2008, there was over a nine-month supply of listings on the market. Today, that number is less than a three-month supply. Here’s a graph showing the difference between the two markets.

Bottom Line

The data indicates why Ivy Zelman, founder of the major housing market analytical firm Zelman and Associates, was on point when she stated:

“The likelihood of us having a foreclosure crisis again is about zero percent.”

With forbearance plans about to come to an end, many are concerned the housing market will experience a wave of foreclosures like what happened after the housing bubble 15 years ago. Here are four reasons why that won’t happen.

1. There are fewer homeowners in trouble this time

After the last housing crash, about 9.3 million households lost their home to a foreclosure, short sale, or because they simply gave it back to the bank.

As stay-at-home orders were issued early last year, the overwhelming fear was the pandemic would decimate the housing industry in a similar way. Many experts projected 30% of all mortgage holders would enter the forbearance program. Only 8.5% actually did, and that number is now down to 3.5%.

As of last Friday, the total number of mortgages still in forbearance stood at 1,863,000. That’s definitely a large number, but nowhere near 9.3 million.

2. Most of the 1.86M in forbearance have enough equity to sell their home

Of the 1.86 million homeowners currently in forbearance, 87% have at least 10% equity in their homes. The 10% equity number is important because it enables homeowners to sell their houses and pay the related expenses instead of facing the hit on their credit that a foreclosure or short sale would create.

The remaining 13% might not all have the option to sell, so if the entire 13% of the 1.86M homes went into foreclosure, that would total 241,800 mortgages. To give that number context, here are the annual foreclosure numbers of the three years leading up to the pandemic:

2017: 314,220

2018: 279,040

2019: 277,520

The probable number of foreclosures coming out of the forbearance program is nowhere near the number of foreclosures coming out of the housing crash 15 years ago. The number does, however, draw a similar comparison to the three years prior to the pandemic.

3. The current market can absorb any listings coming to the market

When foreclosures hit the market in 2008, there was an excess supply of homes for sale. The situation is exactly the opposite today. In 2008, there was a 9-month supply of listings for sale. Today, that number stands at less than 3 months of inventory on the market.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains when addressing potential foreclosures emerging from the forbearance program:

“Any foreclosure increases will likely be quickly absorbed by the market. It will not lead to any price declines.”

4. Those in power will do whatever is necessary to prevent a wave of foreclosures

Just last Friday, the White House released a fact sheet explaining how homeowners with government-backed mortgages will be given further options to enable them to keep their homes when exiting forbearance. Here are two examples mentioned in the release:

“For homeowners who can resume their pre-pandemic monthly mortgage payment and where agencies have the authority, agencies will continue requiring mortgage servicers to offer options that allow borrowers to move missed payments to the end of the mortgage at no additional cost to the borrower.”

“The new steps the Department of Housing and Urban Development (HUD), Department of Agriculture (USDA), and Department of Veterans Affairs (VA) are announcing will aim to provide homeowners with a roughly 25% reduction in borrowers’ monthly principal and interest (P&I) payments to ensure they can afford to remain in their homes and build equity long-term. This brings options for homeowners with mortgages backed by HUD, USDA, and VA closer in alignment with options for homeowners with mortgages backed by Fannie Mae and Freddie Mac.”

When evaluating the four reasons above, it’s clear there won’t be a flood of foreclosures coming to the market as the forbearance program winds down.

Bottom Line

As Ivy Zelman, founder of the major housing market analytical firm Zelman & Associates, notes:

“The likelihood of us having a foreclosure crisis again is about zero percent.”