What To Expect from the Housing Market in the Second Half of 2026

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

Mortgage Rates Could Be Near a Turning Point

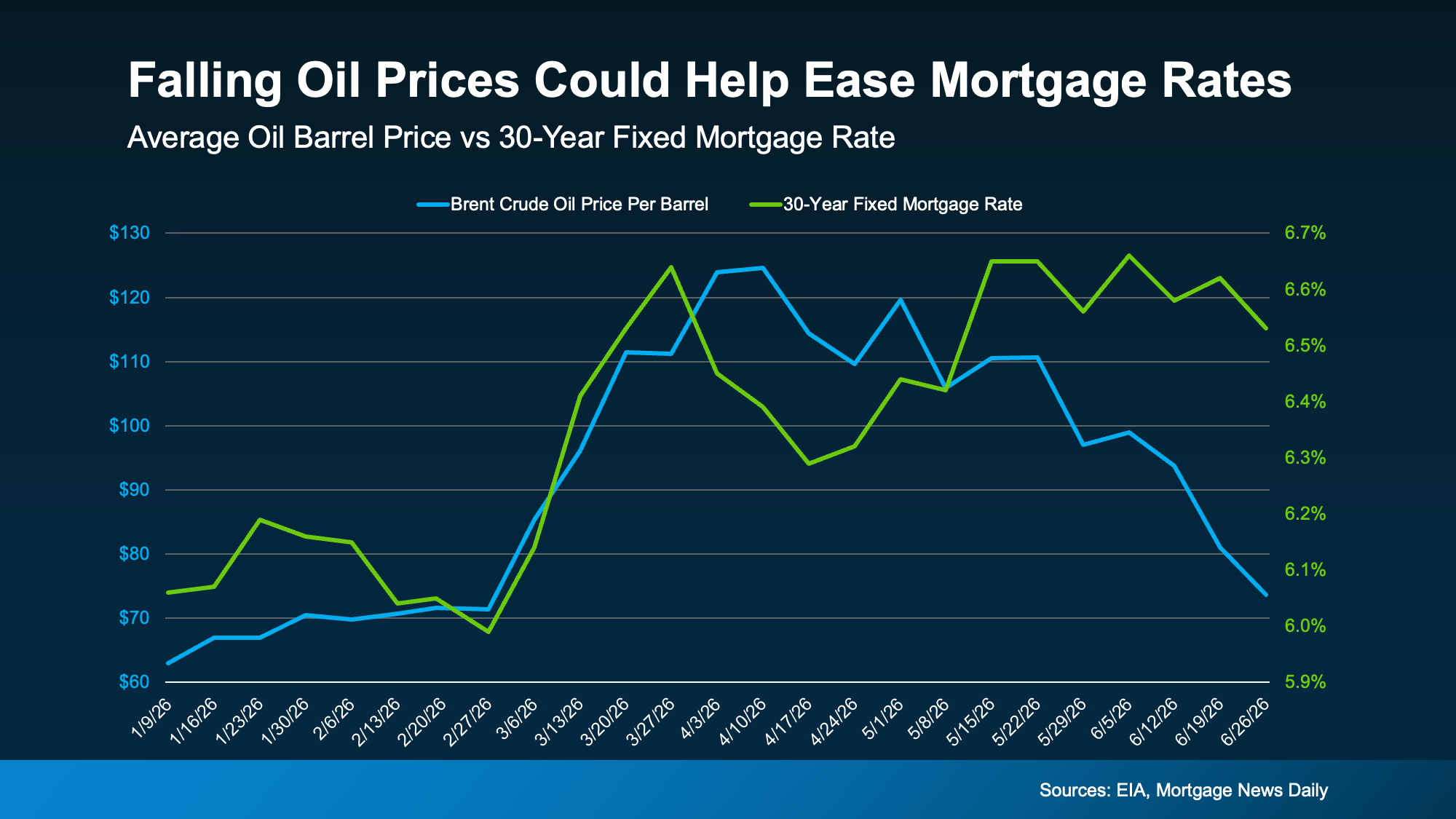

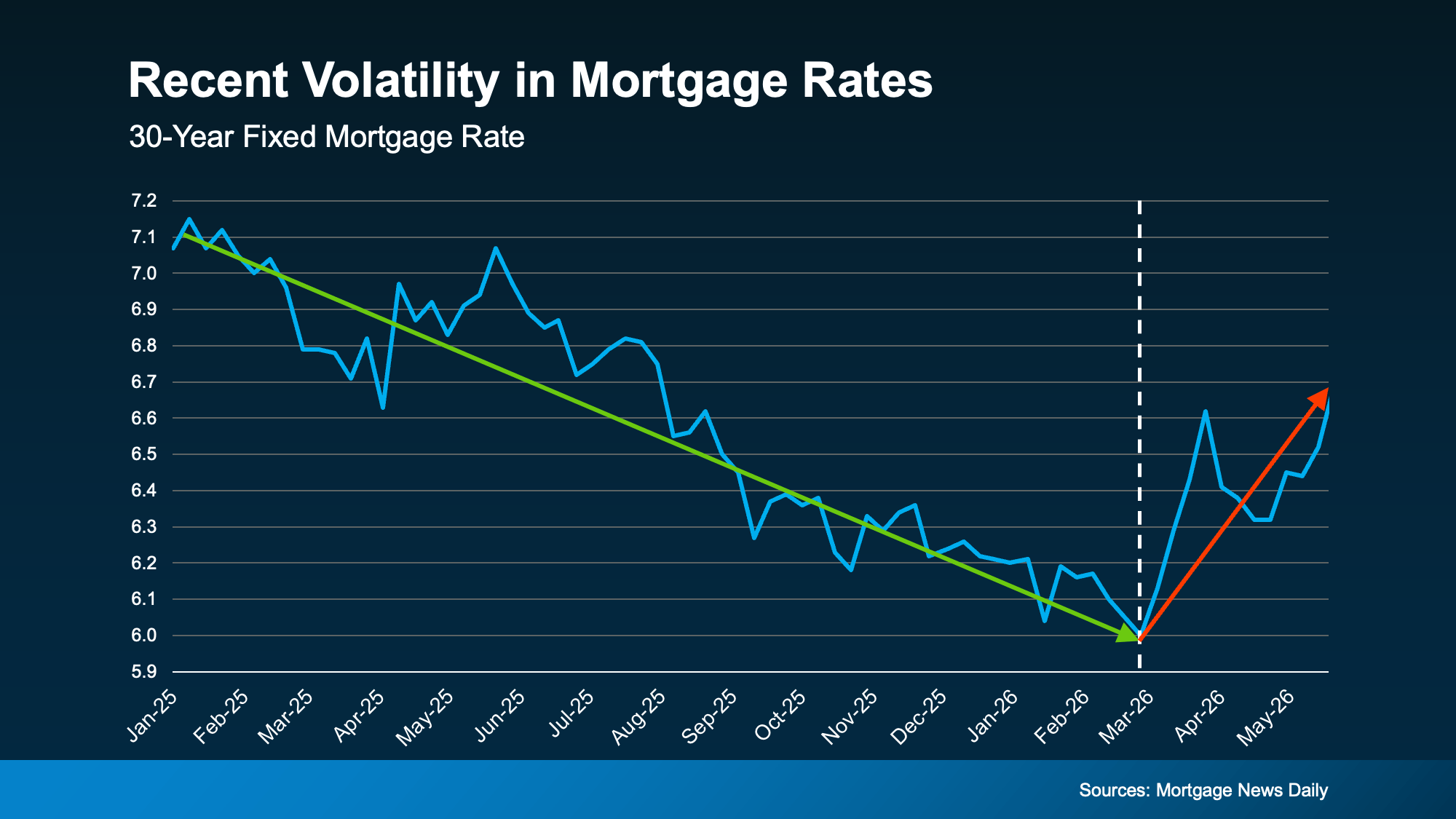

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

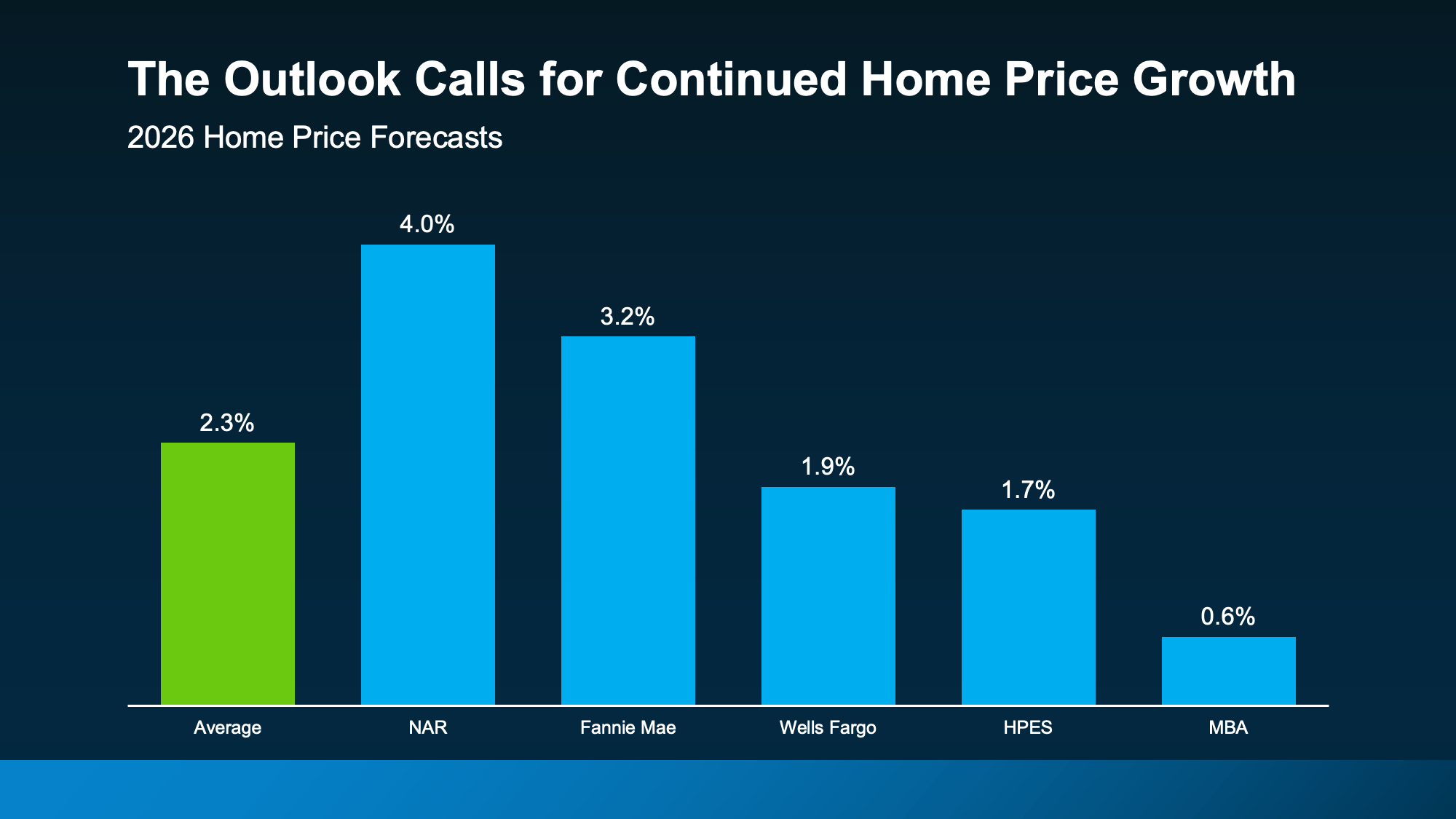

Home Prices Could Pick Back Up

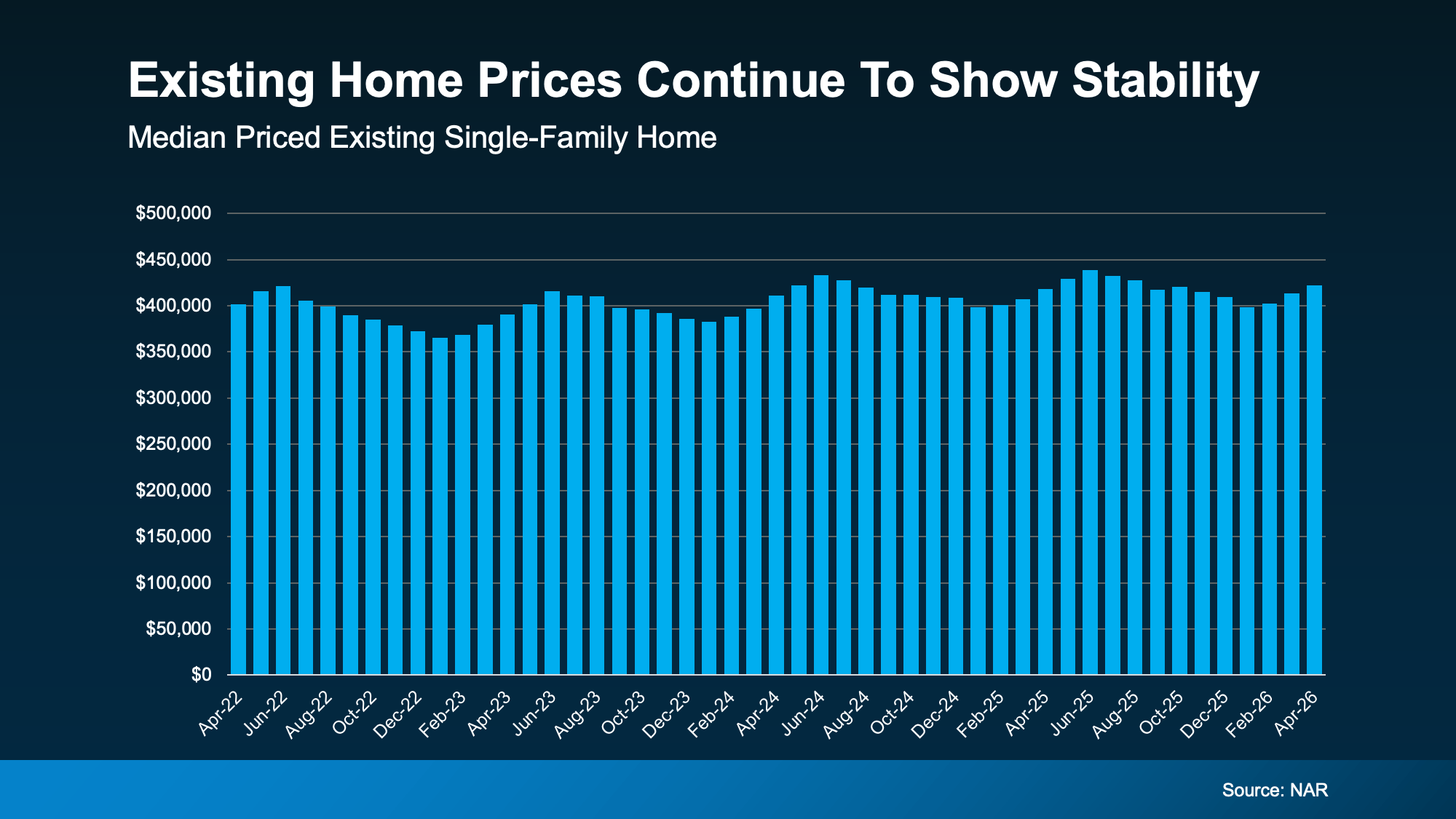

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

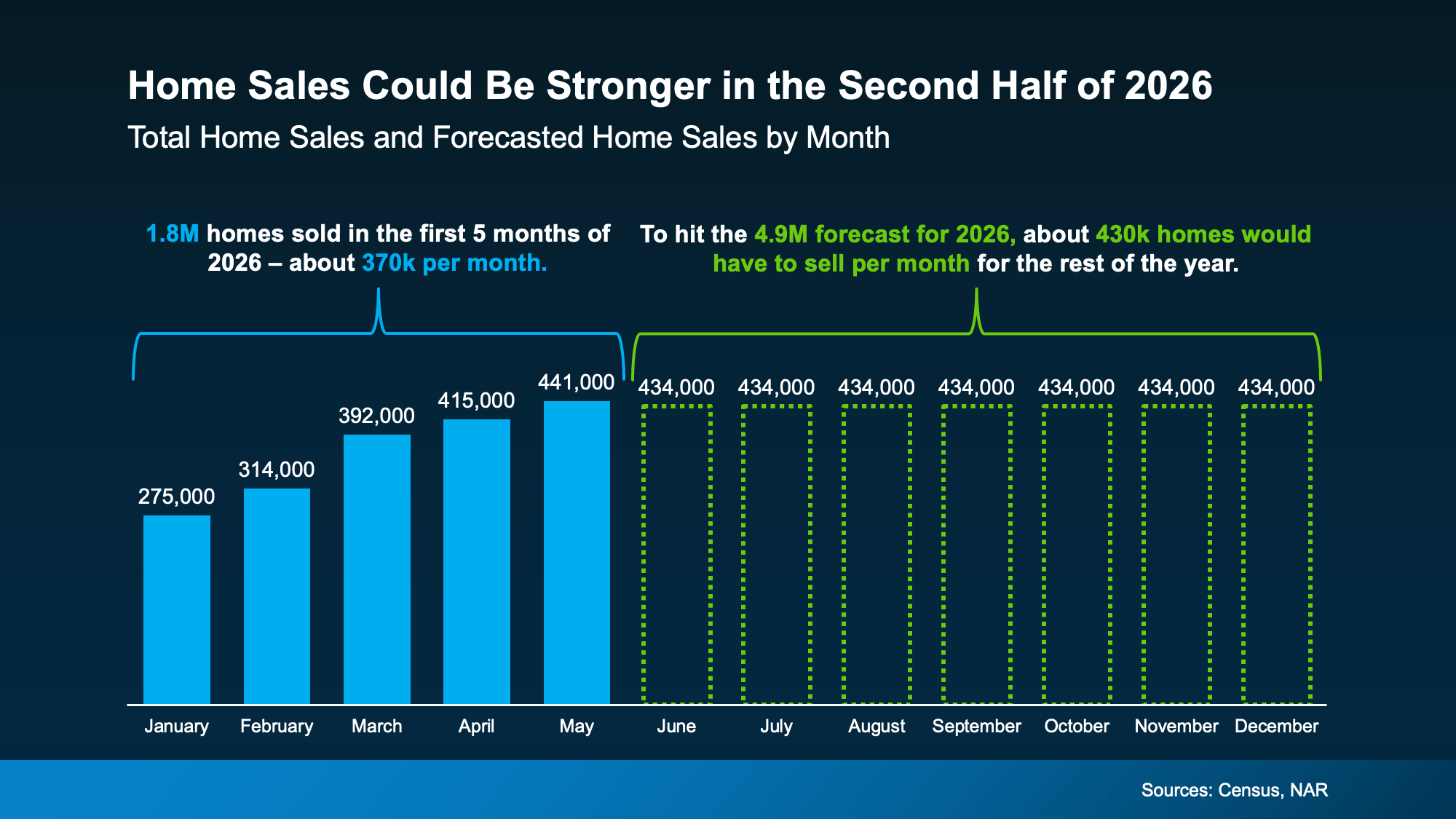

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

Bottom Line

The second half of the year probably won’t be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in your local market, connect with an agent.

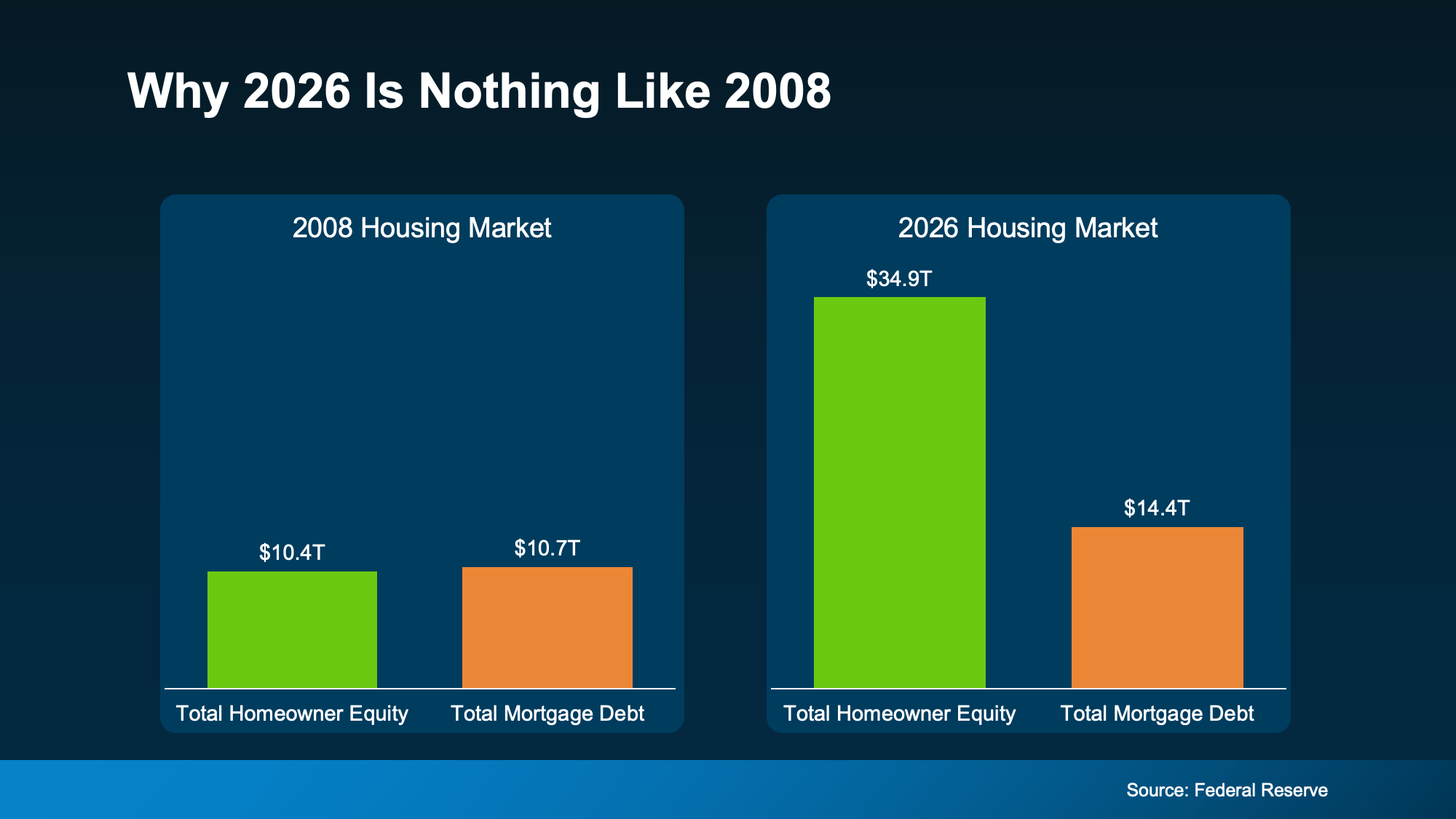

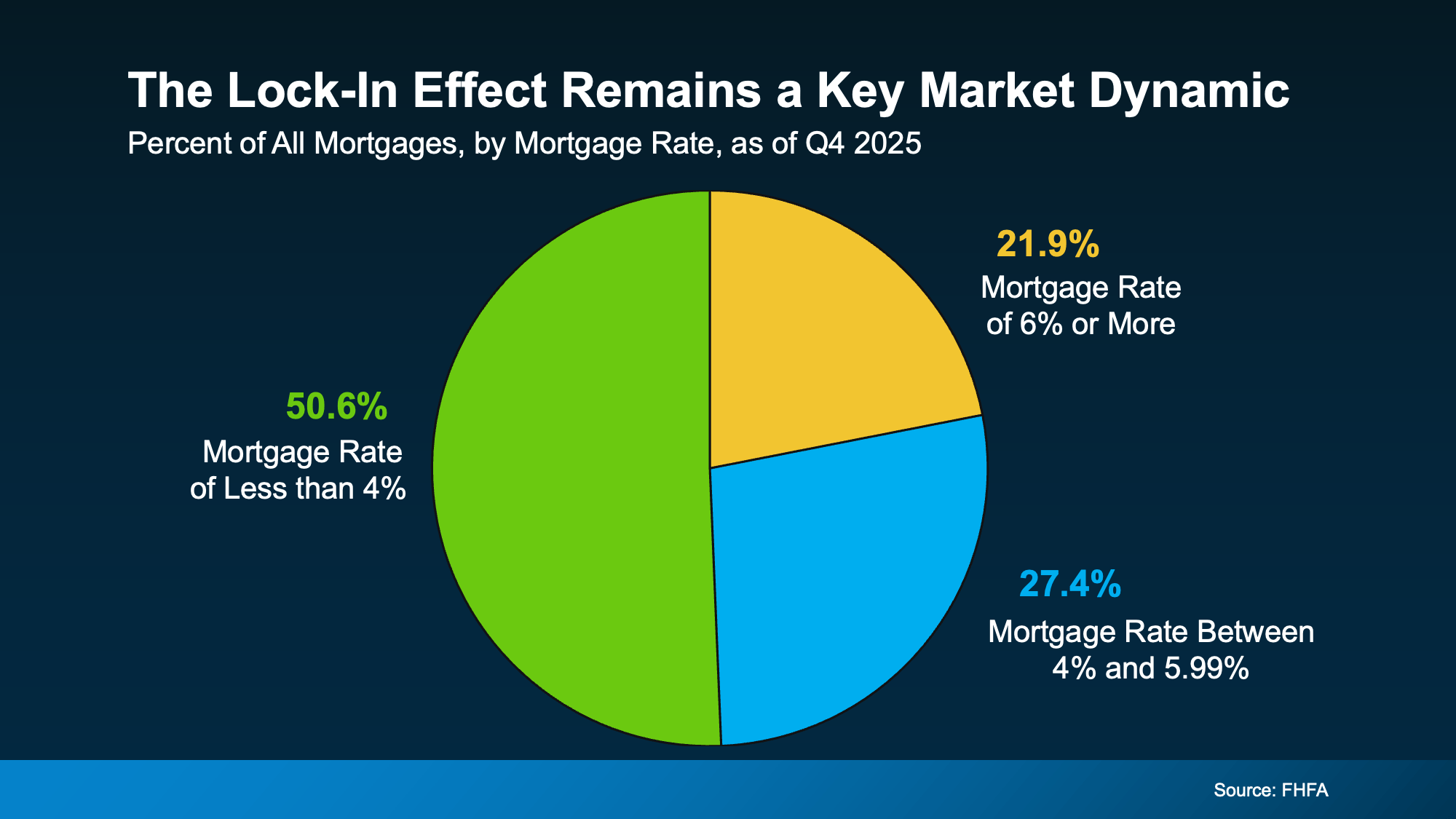

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time. That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling. That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

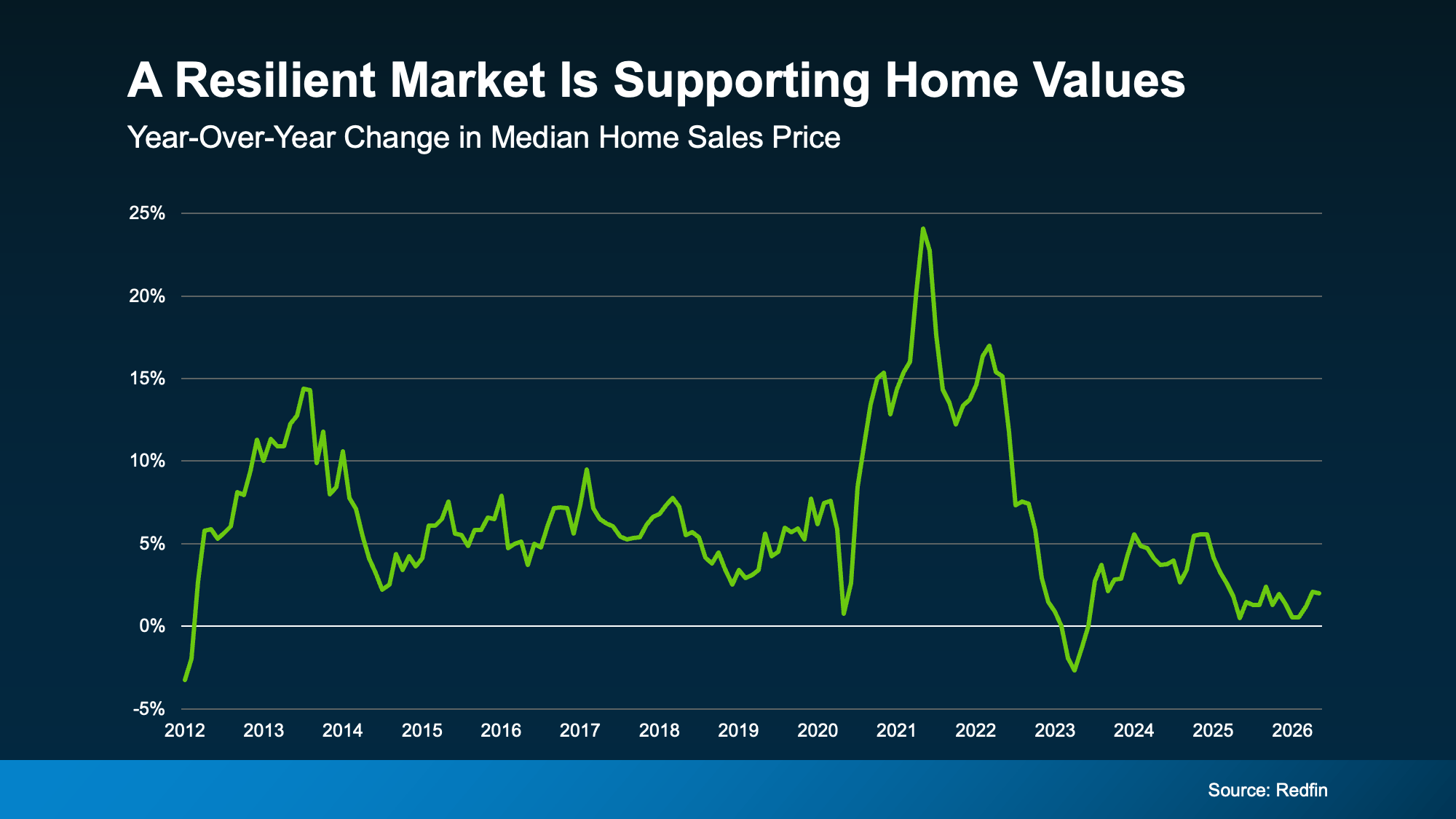

While it can vary a lot based on where you live, only

While it can vary a lot based on where you live, only  That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.