It’s impossible to research the subject of buying a home without coming across a headline declaring that the fall in home affordability is a crisis. However, when we add context to the most recent affordability statistics, we soon realize that, though homes are less affordable than they have been over the last few years, they are more affordable than they historically have been.

Black Knight, a premier provider of data and analytics for the mortgage industry, just released their latest Monthly Mortgage Monitor which includes a new analysis of the affordability situation. Here’s what the report reveals:

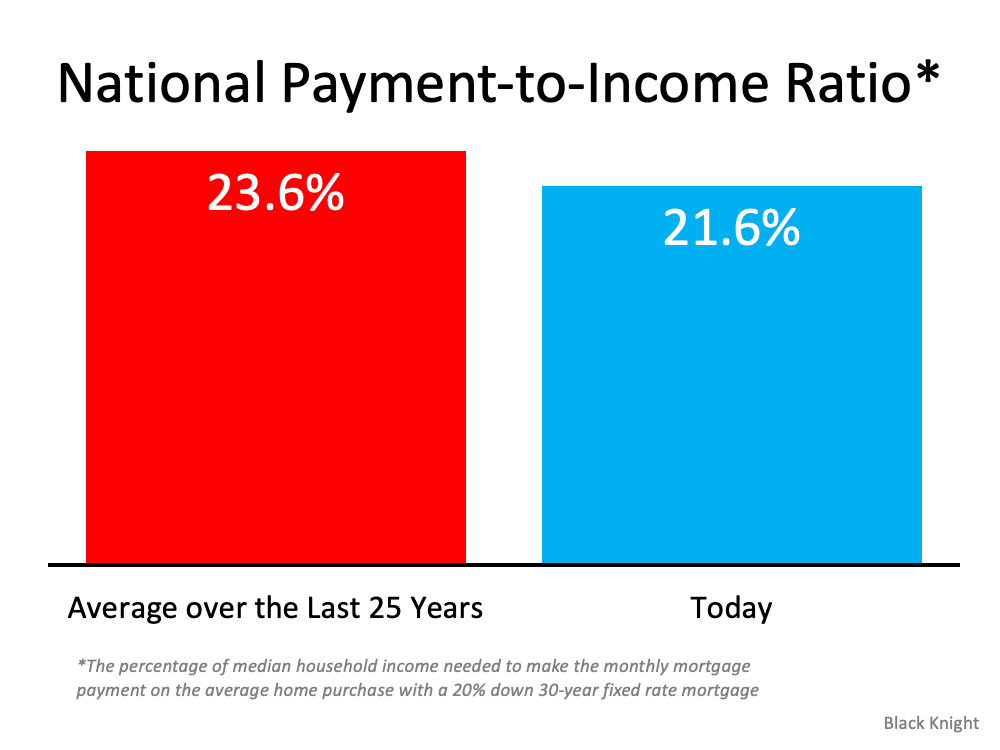

“The monthly payment required to purchase the average priced home with a 20% down 30-year fixed rate mortgage increased by nearly 20% (+$210) over the first nine months of 2021, . . . It now requires 21.6% of the median household income to make the monthly mortgage payment on the average home purchase, the least affordable housing has been since 30-year rates rose to nearly 5% back in late 2018.”

Basically, the report shows that homes are less affordable today than at any other time in the last three years. However, in a previous report earlier this year, Black Knight calculated that the percentage of the median household income to make the monthly mortgage payment on the average home purchase over the last 25 years was 23.6% (see graph below):Today’s payment-to-income ratio is more affordable than the average over the last 25 years. Given that context, we can see that American households still have the same ability to be homeowners as their parents did 20 years ago.

This confirms the recent analysis of ATTOM Data resources where Todd Teta, Chief Product and Technology Officer, explains:

“The typical median-priced home around the U.S. remains affordable to workers earning an average wage, despite prices that keep going through the roof. Super-low interests and rising pay continue to be the main reasons why.”

Bottom Line

It’s true that it’s less affordable to buy a home today than it has been the last few years. However, it’s more affordable to buy today than the average over the last 25 years. In other words, homes are less affordable, but they’re not unaffordable. That’s an important distinction.

Let me start by saying that I am excited for you. The only reason that you would be reading this is because you have determined that owning a home may be right for you. It means that you are at least exploring the possibilities and considering what life would look like as a homeowner. That alone is exciting and a proposition that is full of promise.

Your reading this also means that I have a chance to earn the opportunity to help you to achieve Your Own Personal American Dream. One of the reasons that I love my job is because I get to help people just like you create and shape their lifestyle through homeownership. It is truly an honor when someone allows me that opportunity. So let me share with you how I can help.

All of our services start with a quick 15 – 30 minute coaching call which is a basic introductory consultation. On that call you take out your dream paint brush and start painting a picture of what your American Dream looks like. I will ask you some specific questions about your plans and qualifications and, if we both decide at the end of that call that we should move to the next stage, we will schedule your comprehensive buyer consultation.

Depending on your experience as a homeowner/future homeowner, right off the bat you will notice that my approach is much different than 98% or more of real estate agents that you may have talked to or even worked with in the past. Since 1989 I have been a full time REALTOR® and have had the privilege of helping hundreds of families, couples, and individuals buy and sell homes. I discovered along the way that the more time taken in planning and preparing up front, the more successful the home purchase or sale would be in the end.

As your HousingCoach℠ I will help you to develop and solid home buying game plan which will incorporate your current circumstances and your plans, goals, and dreams for the next 5, 10, or even 20 or more years into the future. Your success as a home buyer can be measured in how well you are equipped and prepared to find the home that best fits your plan, compete against other home buyers, negotiate with the seller from a place of strength, and complete the transaction with as few hassles as possible.

Once we decide to work together I will help you to build out your Home Buying Game Plan, assemble your Home Buying Real Estate Team, structure and activate an automated Home Search Process, prepare you to have the best competitive advantage, negotiate on your behalf to get the best possible deal, and coordinate all of the transaction requirements and activities until the deal is closed.

My goal is that in the process of helping you to achieve Your Personal American Dream, that you are provided a personal level of service such that you feel compelled to refer me and my services to your family, friends, co-workers, and people you care about. That is how I will know I did my job well.

The best advice carries across multiple areas of life. When it comes to homebuying, a few simple tips can help you stay on track.

Because of increased demand, you’ll need to be patient and embrace compromises during your search. Then, once you’ve fallen in love, commit by putting your best offer forward.

If you’re looking to buy a home this year, let’s connect so you have a dedicated partner and teammate to help you find the one.

Today’s housing market is truly one for the record books. Over the past year, we’ve seen the lowest mortgage rates in history. And while those rates seemed to bottom out in January of this year, the golden window of opportunity for buyers isn’t over just yet. If you’re one of the buyers who worry they’ve missed out, rest assured today’s mortgage rates are still worth taking advantage of.

Even today, our mortgage rates are below what they’ve been in recent decades. So, while you may not be able to lock in the rate your friend got recently, you’re still in a great position to secure a rate well below what your parents and even grandparents got in years past. The key will be acting sooner rather than later.

In late September, mortgage rates ticked above 3% for the first time in months. And according to experts throughout the industry, mortgage rates are projected to continue rising in the months ahead. Here’s where experts say rates are headed:While a projected half percentage point increase may not seem substantial, it does have an impact when you’re buying a home. When rates rise even slightly, it affects how much you’ll pay month-to-month on your home loan. The chart below shows how it works:In this example, if rates rise to 3.55%, you’ll pay an extra $100 each month on your monthly mortgage payment if you purchase a home around this time next year. That extra money can really add up over the life of a 15 or 30-year loan.

Clearly, today’s mortgage rates are worth taking advantage of before they climb further. The rates we’re seeing right now give you a unique opportunity to afford more home for your money while keeping your monthly payment down.

Bottom Line

Waiting for a lower mortgage rate could cost you. Experts project rates will continue to rise in the months ahead. Let’s connect so you can seize this opportunity before they increase further.

A recent survey from LendingTree.com found there are multiple reasons why Americans would choose to purchase a home instead of renting. Some of the most popular non-financial reasons given include:

The flexibility to make the space your own

The pride homeownership offers

The sense of stability

In the same survey, 41% of respondents say they’d rather own a home than rent because of the unique way homeownership builds wealth over time.

And experts agree – the home you own is an important tool for building your net worth. Here’s what many of those experts have to say about building long-term financial stability through homeownership.

“Homeowners who purchased a typical single-family existing-home 30 years ago at the median sales price of $103,333 with a 10% down payment loan and who sold the property at the median sales price of $357,700 in 2021 Q2 accumulated housing wealth of $349,258, . . .”

Mark Fleming, Chief Economist at First American, points out that a home is truly a one-of-a-kind asset. It’s the only asset that’s both an investment and a place for you to call your own.

“The major financial advantage of homeownership is the accumulation of equity in the form of house price appreciation. . . . We won’t always have 17% house price appreciation, but we have to take into account the fact that the shelter that you’re owning is an equity-generating or wealth-generating asset.”

Homeowners can leverage the wealth they generate in several ways throughout their life. Tapping into accumulated equity has long been used to pay for the cost of an education, to start a business, or to fund various other expenses. The Joint Center of Housing Studies at Harvard points out:

“. . . by paying down mortgage principal each month and participating in the long-term appreciation of home values, a family can build wealth that can be used for retirement or other needs, including helping the next generation.”

Bottom Line

With home prices expected to continue to appreciate in coming years, homebuyers have an opportunity to start the long-term wealth-building process right now. Let’s connect today if you’re ready to begin your journey on the path to becoming a homeowner.

The financial benefits of buying a home versus renting one are always up for debate. However, one element of the equation is often ignored – the ability to build wealth as a homeowner.

According to the latest research from the National Association of Realtors (NAR):

“Homeownership is a key pathway to building wealth and narrowing the racial income and wealth inequality gap. Housing wealth (equity) accumulation takes time and is built up by price appreciation and paying off the mortgage.”

An increase in equity builds the wealth of the individual that owns it. This wealth can be passed down to future generations. The Federal Reserve in an addendum to their Survey of Consumer Finances explains:

“There are numerous ways families can transmit wealth and resources across generations. Families can directly transfer their wealth to the next generation in the form of a bequest. They can also provide the next generation with inter vivos transfers (gifts), for example, providing down payment support to enable a home purchase or a substantial wedding gift.”

The Federal Reserve also explains another way wealth (including the additional net worth generated by an increase in home equity) can benefit future generations:

“In addition to direct transfers or gifts, families can make investments in their children that indirectly increase their wealth. For example, families can invest in their children’s educational success by paying for college or private schools, which can in turn increase their children’s ability to accumulate wealth.”

Here’s a look at how equity can build your wealth over time when you own a home.

Equity over the Last 30 Years

The NAR research reveals that the average gain for homeowners over the last five years was $139,134 and over the last 10 years was $218,505. Looking even further back in time, the article says:

“Homeowners who purchased a typical single-family existing-home 30 years ago at the median sales price of $103,333 with a 10% down payment loan and who sold the property at the median sales price of $357,700 in 2021 Q2 accumulated housing wealth of $349,258.”

Homeownership builds household wealth which also enables households to more easily move to the home of their dreams. As Mark Fleming, the Chief Economist at First American,explains:

“As homeowners gain equity in their homes, they are more likely to consider using that equity to purchase a larger or more attractive home – the wealth effect of rising equity.”

If you missed out on the equity gains over the last 30 years, don’t fret. Experts are still calling for substantial growth in equity over the next five years.

Looking Forward at the Equity To Come

The most recent Home Price Expectation Survey, a survey of over one hundred economists, real estate experts, and investment and market strategists, expects home values (and therefore equity) to increase as follows:

2021: 11.74%

2022: 5.82%

2023: 3.94%

2024: 3.56%

2025: 3.55%

The survey estimates a 31.8% cumulative appreciation over the next five years. Using their annual projections, the graph below shows the equity build-up a purchaser could earn, using a $350,000 home as an example:That’s a potential increase in household wealth of $111,285 over five years.

Bottom Line

Owning a home is one of the best ways to grow your wealth over time. House wealth can impact generations. In many cases, the largest single investment a household has is their home. As that investment appreciates in value, the financial options also increase.

Today’s payment-to-income ratio is more affordable than the average over the last 25 years. Given that context, we can see that American households still have the same ability to be homeowners as their parents did 20 years ago.

Today’s payment-to-income ratio is more affordable than the average over the last 25 years. Given that context, we can see that American households still have the same ability to be homeowners as their parents did 20 years ago.

![Homebuyer Tips for Finding the One [INFOGRAPHIC]](https://housingcoach.com/wp-content/uploads/2021/10/20211015-KCM-Share-549x300-1.png)

![Homebuyer Tips for Finding the One [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/10/14130433/20211015-MEM-1046x2057.png)