4 Reasons Your House Is High on Every Buyer’s Wish List This Season

When the holidays roll around, travel plans, family gatherings, and all the chaos of the season may make you think it’s better to pull your listing off the market or to wait until 2026 to sell your house. But here’s the thing.

Waiting could mean missing out on a great window of opportunity. Because while other sellers are stepping away, you can lean in – and that might actually give you the edge. Here are 4 reasons selling now may be the better bet.

1. Buyers This Time of Year Are Serious

Don’t let the season fool you. While casual browsers tend to step back around the holidays, serious buyers stay in the game. The people looking for homes right now usually aren’t just browsing. They’re ready to make a move and they usually want to close before the new year. As Zillow says:

“While more buyers have tended to shop in the spring and summer months, those shopping in the winter are likely to be motivated — often moving because of a job relocation, change in financial situation, or change in family needs.”

Their timelines are real and missing them would create a hassle for the buyer, so they’re eager to get the deal done. And that’s exactly the kind of buyer you want to work with.

2. You Have Control Over Your Schedule (and Showings)

Some homeowners decide not to sell this time of year because they don’t want to juggle showings during the holiday rush. They’re anticipating traveling to see family and thinking about buyers in their home only adds another layer of complexity.

But here’s what no one’s reminded them. You can control your showings and can set times that work for your schedule. You don’t have to stop your plans to keep your sale on track. The right agent can help you manage your calendar, your showings, and your stress level.

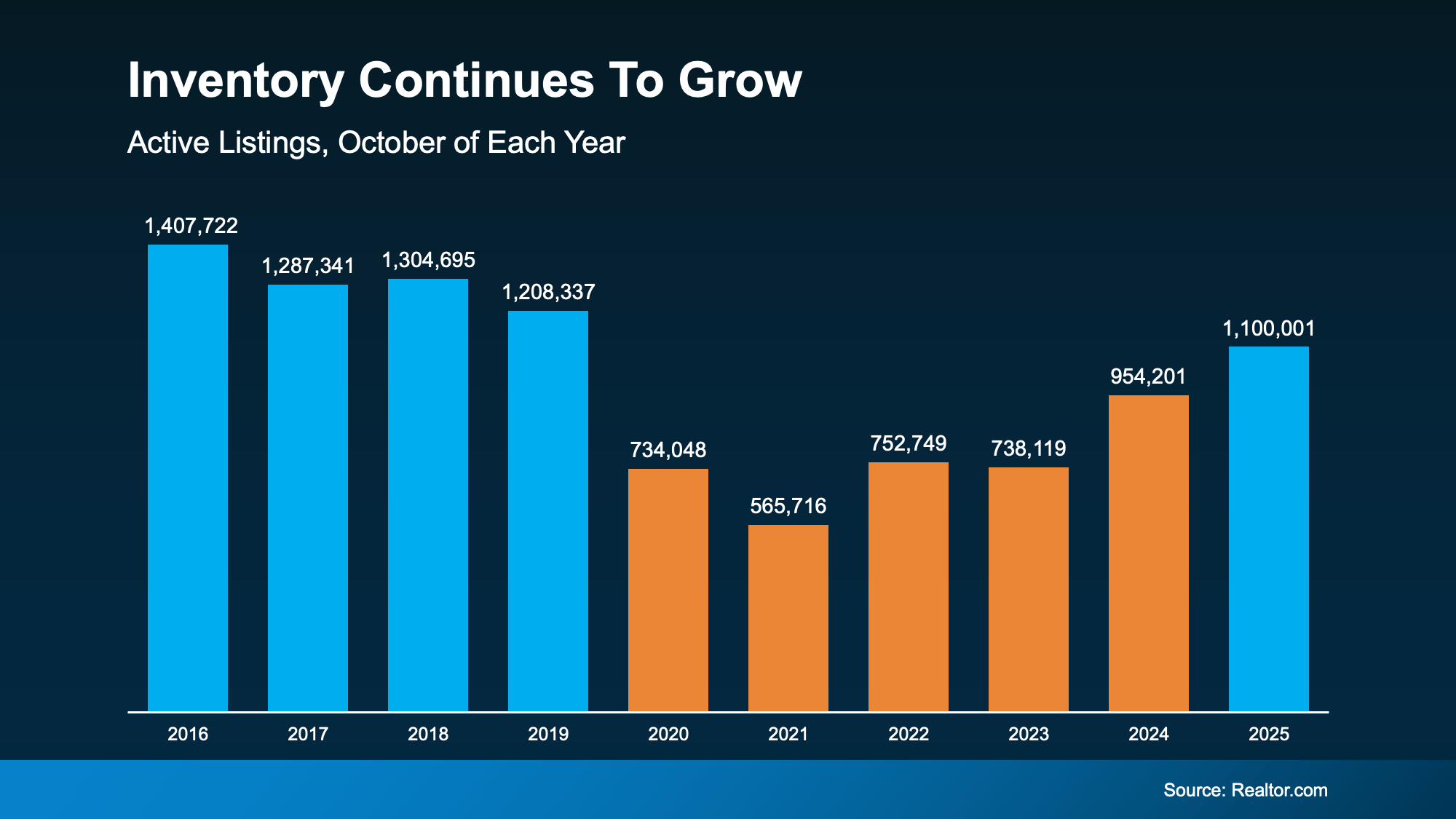

3. Other Sellers May Step Back, Which Means Less Competition

Because fewer sellers tend to list this time of year, the number of homes for sale usually falls a bit. Lisa Sturtevant, Chief Economist at Bright MLS, explains:

“As we approach the end of the year, listing activity tends to slow and would-be sellers decide to wait until after the new year to list . . .”

And in a year when inventory has been steadily rising, that seasonal slowdown works in your favor. With the potential for fewer sellers on the market, your house will stand out. So, a seasonal dip in listings could help you get noticed, especially if your home is priced right and presented well.

4. Homes Decorated for the Holidays Can Feel More Inviting

You may not realize it, but seasonal decor can actually help you appeal to buyers. Maybe it’s that they have an easier time picturing themselves making memories in the home. Maybe it just feels cozier and more inviting. Whatever the reason, it works. Sometimes tasteful seasonal touches can make it easier to sell your house.

But don’t go overboard. Keep your choices simple to let your home’s charm shine through.

Bottom Line

There are plenty of good reasons to put (or keep) your house on the market during this time of year.

If you want to talk strategy for how to make the most of this season in your market, connect with a local agent.