Are Home Prices Dropping? Here’s the Real Story.

You’ve probably seen posts on social media talking about how “home prices are falling.” And when you see something like that, it’s normal to wonder:

Is this the start of a crash?

What does this mean for my house?

Let’s clear this up right away. This is not a crash. And your home is not suddenly losing a lot of value.

The National Story – Prices Are Still Going Up

Here’s what often gets left out of what you’re seeing online. While some markets are experiencing slight declines, they’re the minority. Most places are still seeing prices rise or at the very least, hold steady.

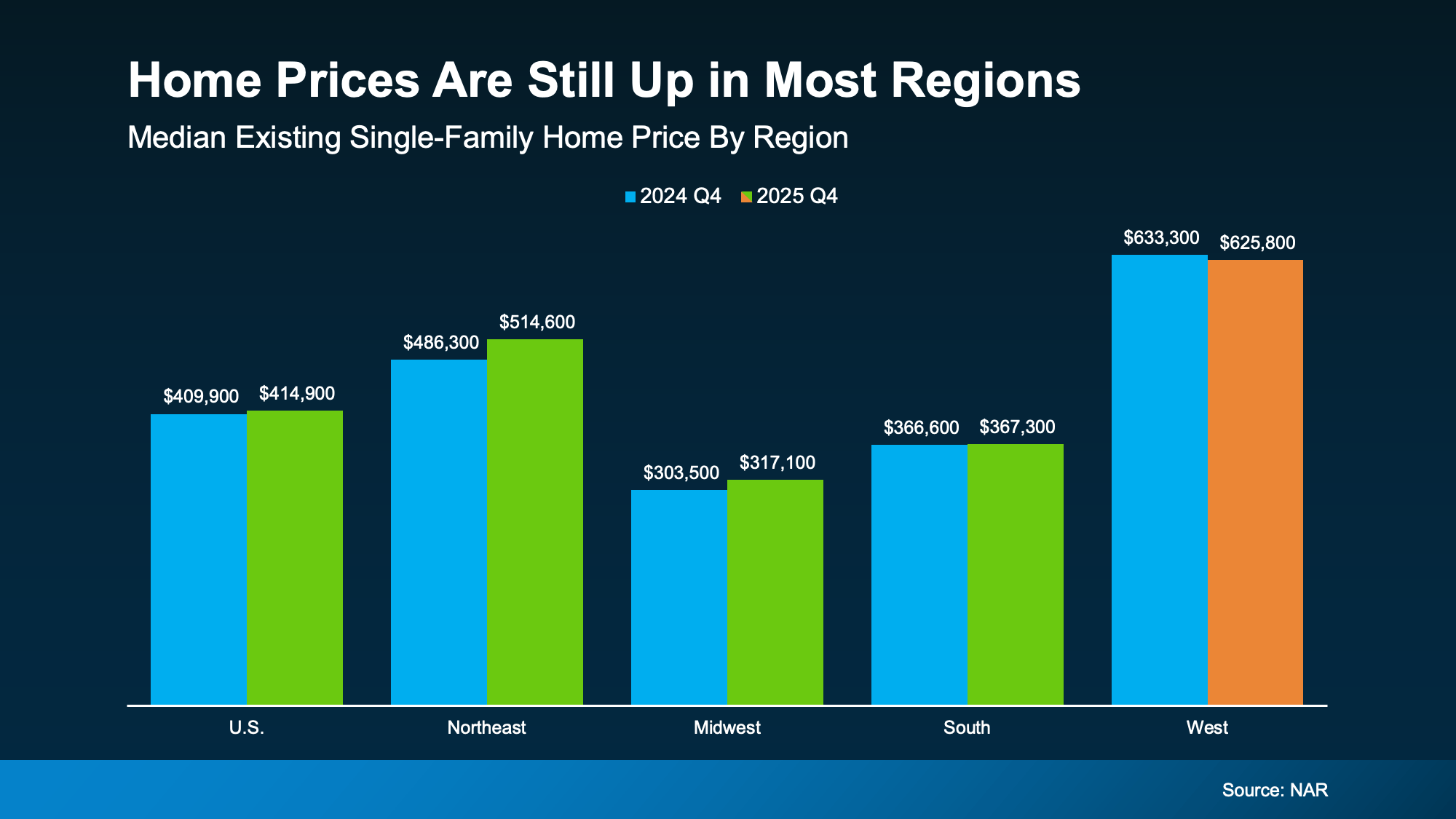

That’s why, at the national level, home prices are still rising, just at a slower pace. According to the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s not the rapid growth of a few years ago, but it’s not a downturn either. And just to really drive this home, here’s a look at the data from NAR at a regional level, so you can see that the negative narrative spun up online isn’t the whole truth (see graph below):

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

There is no wave of falling prices across the country. Instead, there are just a few pockets adjusting after several years of what’s typically considered unsustainable or exponential growth.

Yes, Some Markets Have Come Down, But Look at the Bigger Picture.

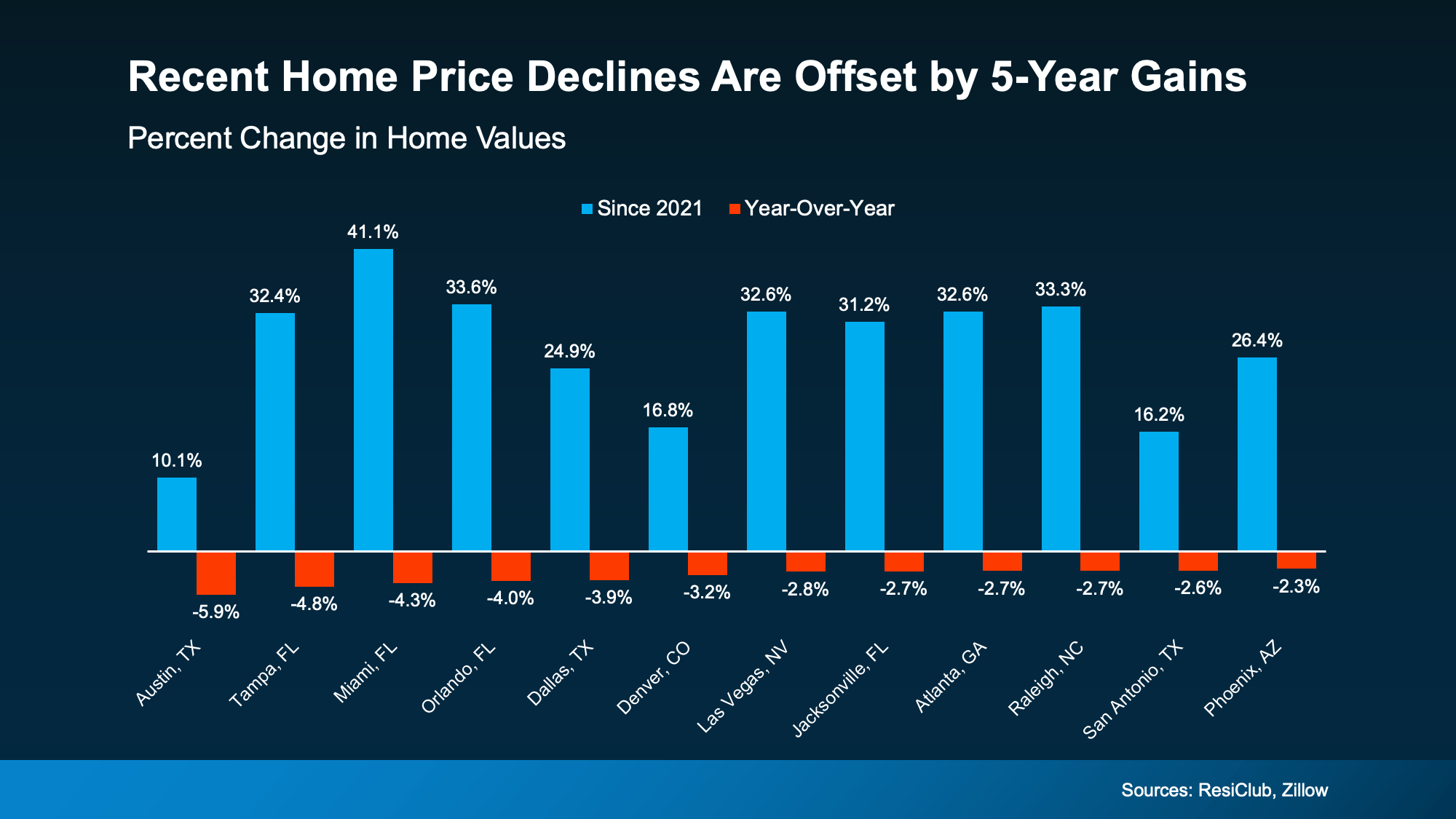

Okay, but what about the places where prices have declined? According to ResiClub and Zillow, that’s not a cause for major concern. When you zoom out and look at those same markets over the past five years, the story changes (see graph below):

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

Online chatter tends to shine a spotlight on the few areas that are down. But the bigger picture shows most homeowners are still in a very strong position.

Of course, every market, and every home, is different. But broadly speaking, home values are holding steady. And this isn’t a sign of widespread trouble in the market.

Bottom Line

Despite what you may be seeing online, home prices are rising or holding steady in most parts of the country.

If you’re curious what your home is worth today, take a look at the numbers with a local real estate agent. Because context, and local expertise, matter more than what you’re seeing online.

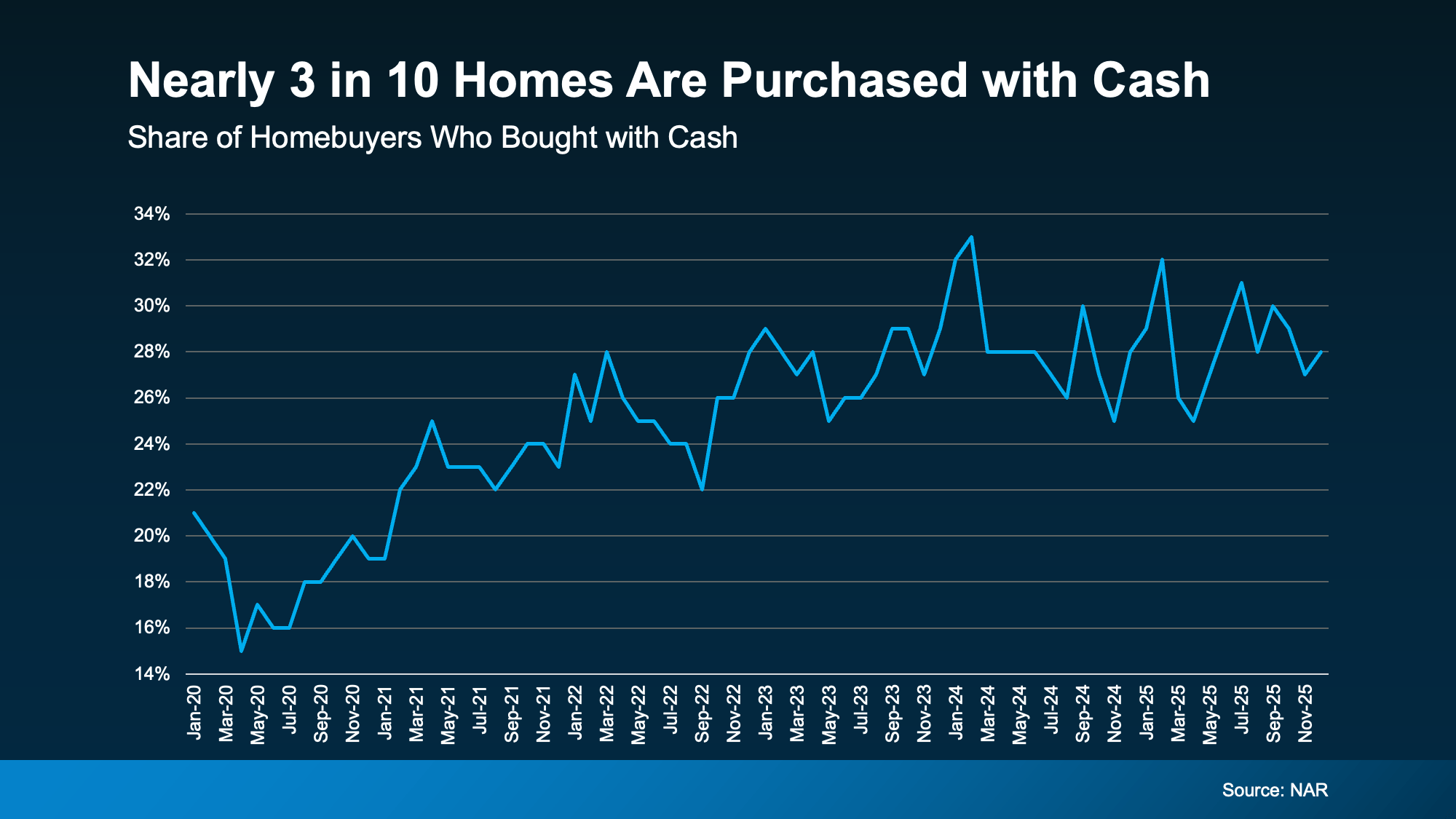

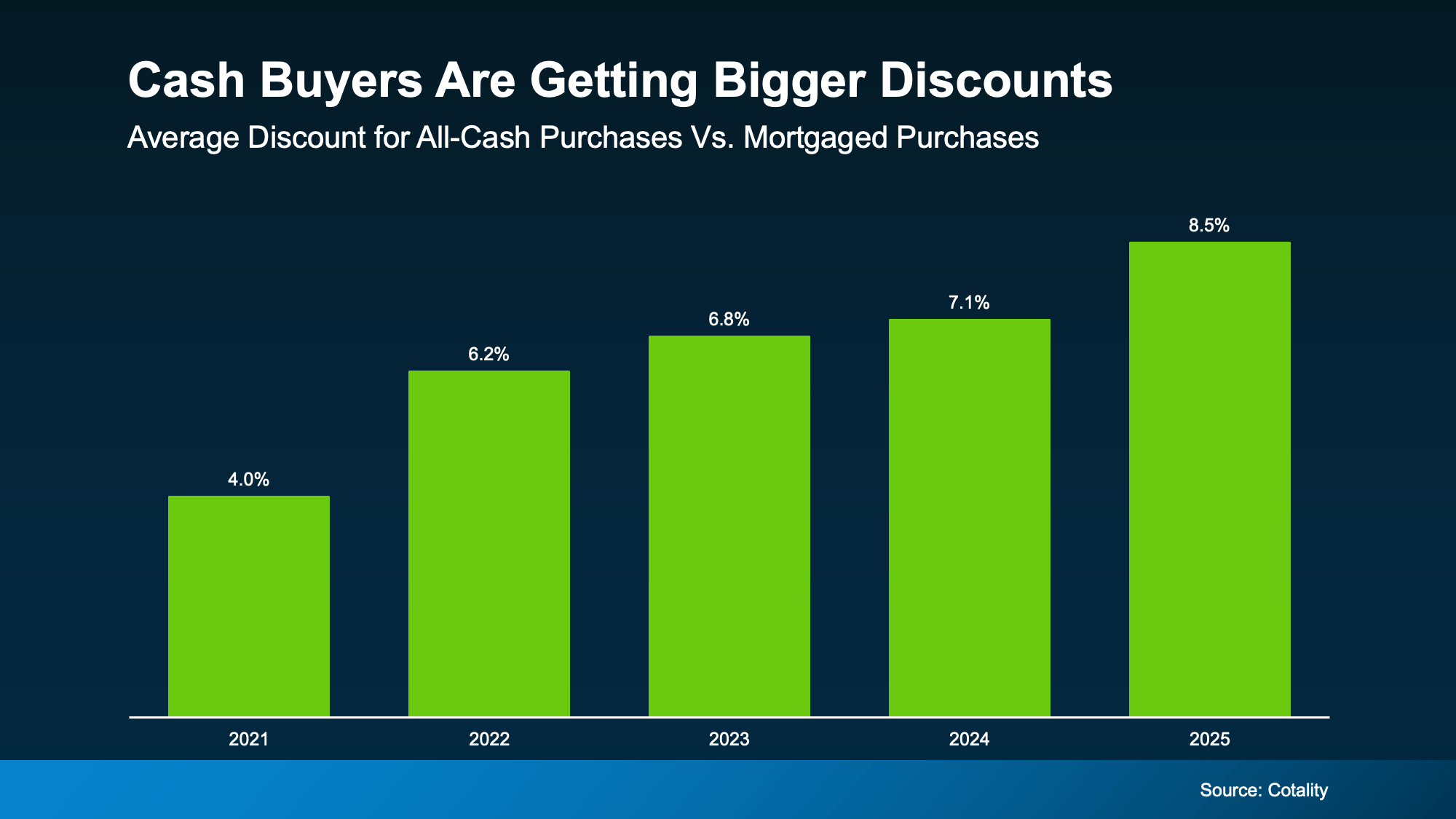

So, how are so many buyers pulling that off? The answer is simple:

So, how are so many buyers pulling that off? The answer is simple:  Is an All-Cash Move Realistic for You?

Is an All-Cash Move Realistic for You?