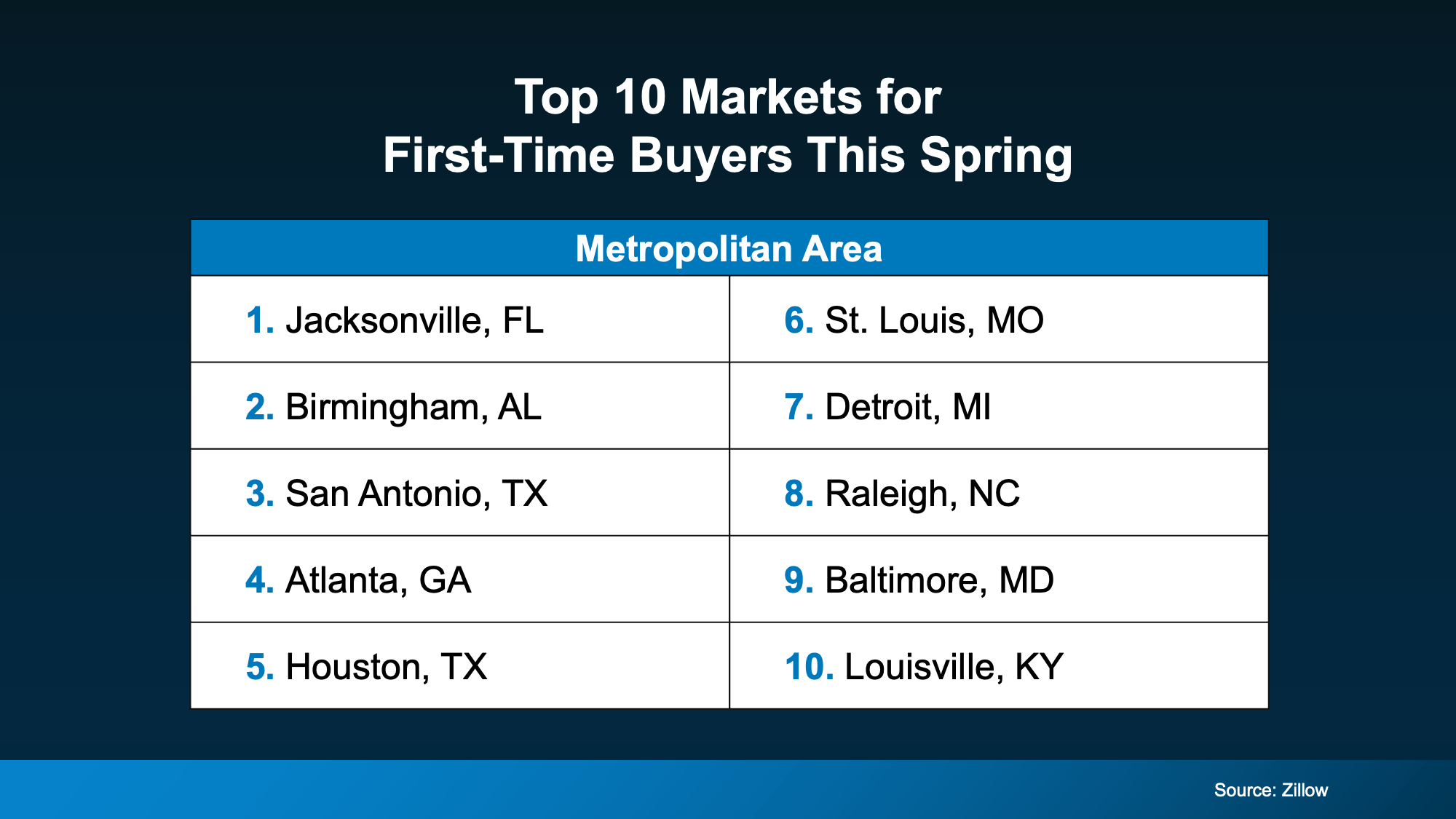

Newly Built Home Prices Hit a 5-Year Low

If you’ve always assumed a newly built home is just not in your budget, you should know the math just got a little friendlier.

The median sale price of a newly built home is now at its lowest level since 2021, according to the latest data from the Census. And on top of that, builders are still rolling out incentives to bring buyers through the door.

Here’s what’s happening, and what it means if you’re shopping right now.

Prices on Newly Built Homes Have Come Down

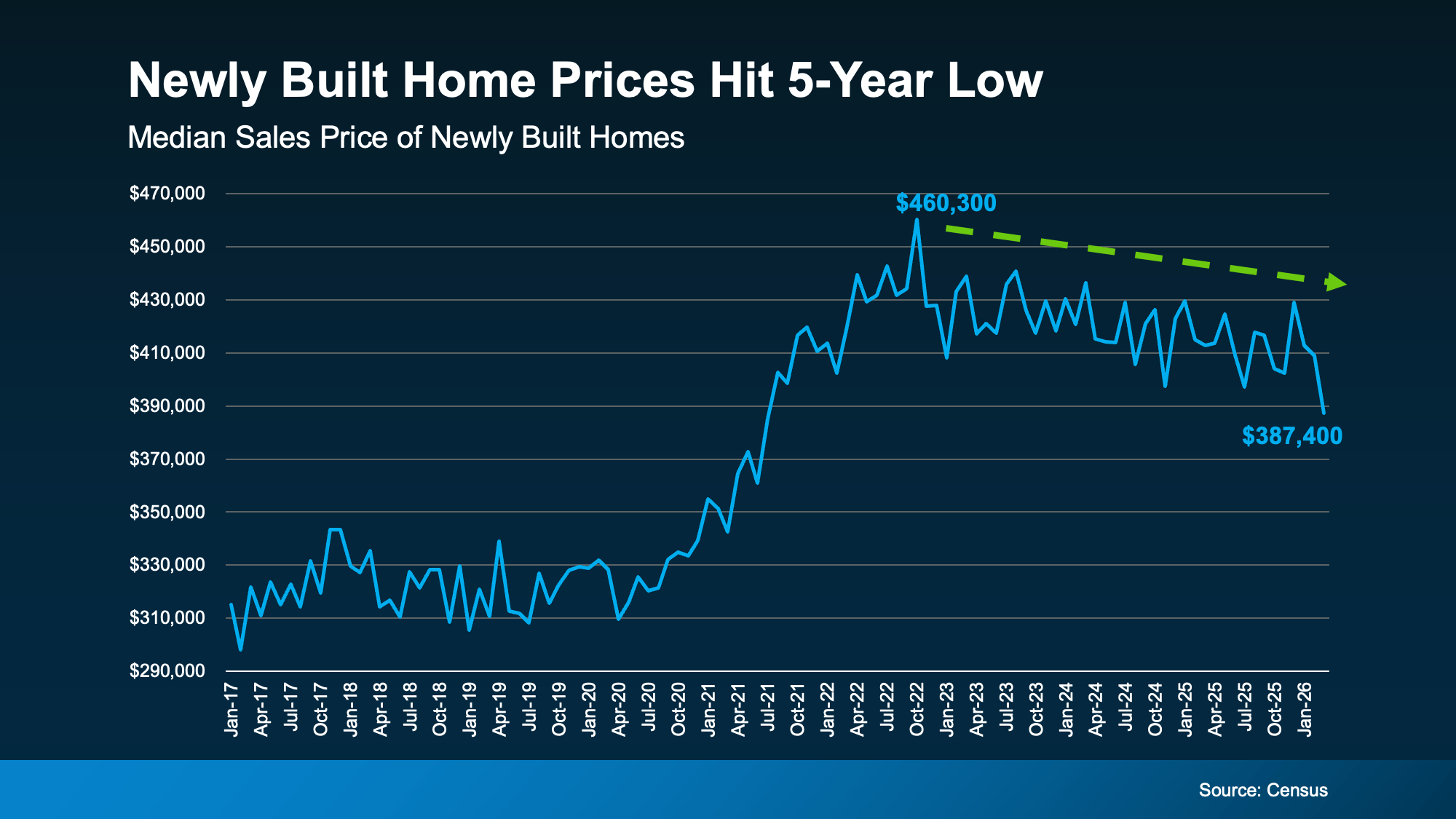

After a steep climb during the pandemic years, prices have eased a bit. The median sale price of newly built homes is sitting at about $390,000. That’s the lowest it’s been in nearly five years (see graph below):

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

That doesn’t mean every home in every market is suddenly affordable. But it does mean that, broadly, you’ll see the best prices on new builds since 2021, if you’re buying now.

Why This Isn’t a Repeat of 2008

And just in case you’re thinking it, lower prices don’t mean the new home market is in trouble. Builders today are being intentional about how much inventory they have, so it doesn’t pile up the way it did in 2008.

If you look back up at the graph, you’ll see that even after the recent improvement in new home prices, they’re still higher than pre-pandemic norms. So, this isn’t a crash. It’s a builder strategy to keep inventory moving.

Homebuilders Are Still Sweetening the Deal

Lower sticker prices aren’t the only break buyers are getting. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers. Those typically include:

- Help with closing costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

- Extra upgrades: Think premium finishes, appliance packages, and designer features, often added at no extra cost.

- Mortgage rate buydowns: When the builder pays to lower your mortgage rate, which reduces your monthly payment.

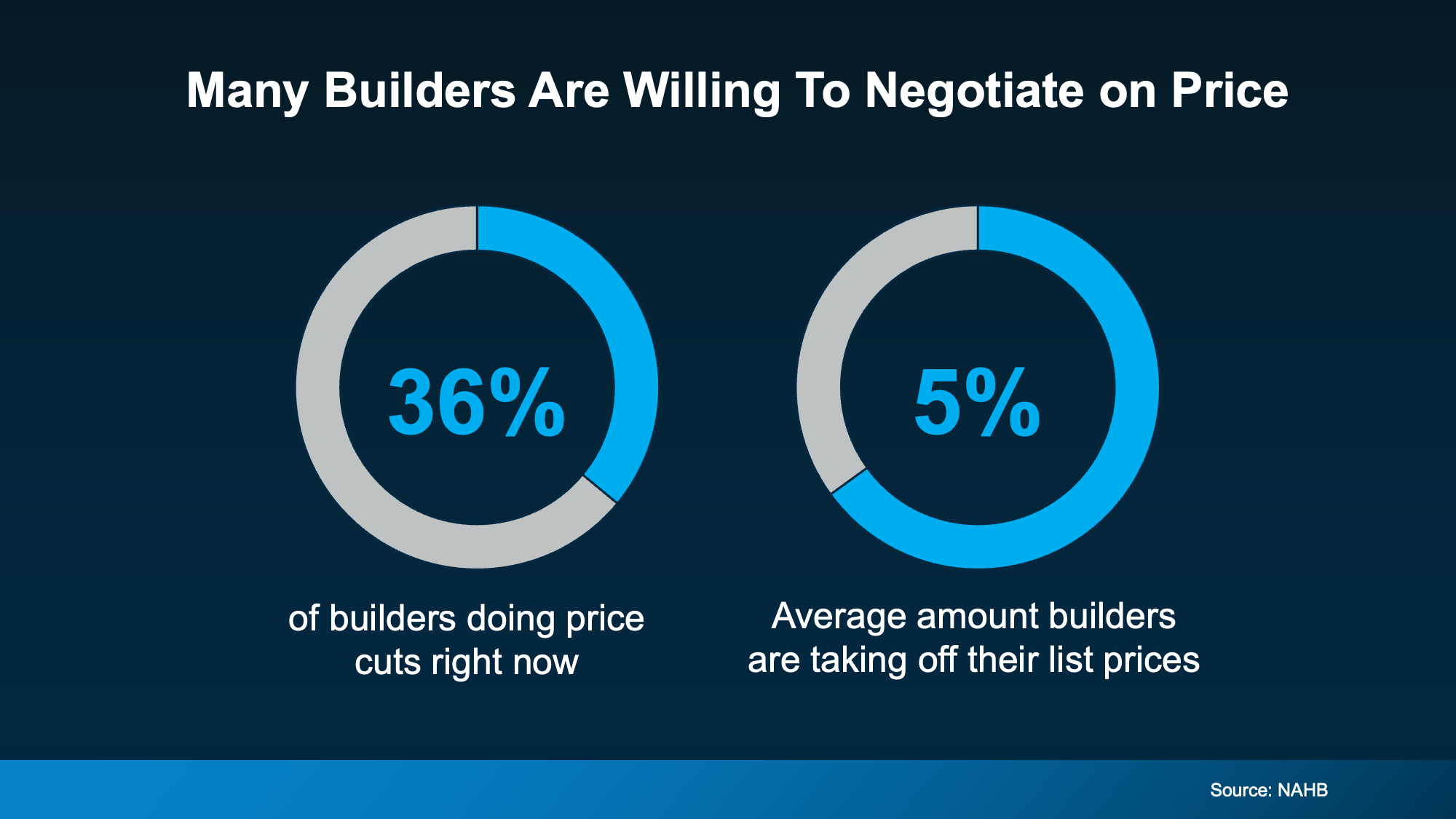

- Price cuts: Over one in three builders (36%) are cutting prices right now, averaging about 5% off list price (see graph below):

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

But builders need to move what they’ve built. That’s a different mindset than a homeowner deciding whether to budge on price. So, you may find they’re more open to adjusting the price than you’d think. As Joel Berner, Senior Economist at Realtor.com, puts it:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

And if you use the version of the graph that shows 2008 prices, you can even reference that in this explainer.

And if here, should I change the last sentence of the lede?

Bottom Line

Builder incentives and lower new home prices are working to your advantage in a way they haven’t in years. Connect with a local real estate agent to see what’s available in your area and what kind of deal a builder may be willing to make.

Why It Works

Why It Works