Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

When your house sits on the market longer than expected, it can get frustrating fast.

You start asking: what now? And for a growing number of homeowners, that turns into: should I just rent it instead?

While it sounds like a simple backup plan, becoming “accidental landlord” is actually a much bigger decision than most people realize. That’s when someone planned to sell, didn’t get the price or traction they hoped for, and decided to rent the house out instead.

And lately, that’s happening more often.

Why the Number of Accidental Landlords Is Rising

If you’re faced with the same choice to rent or to sell, here’s what you need to know. First, you’re not alone. And that should actually be some comfort.

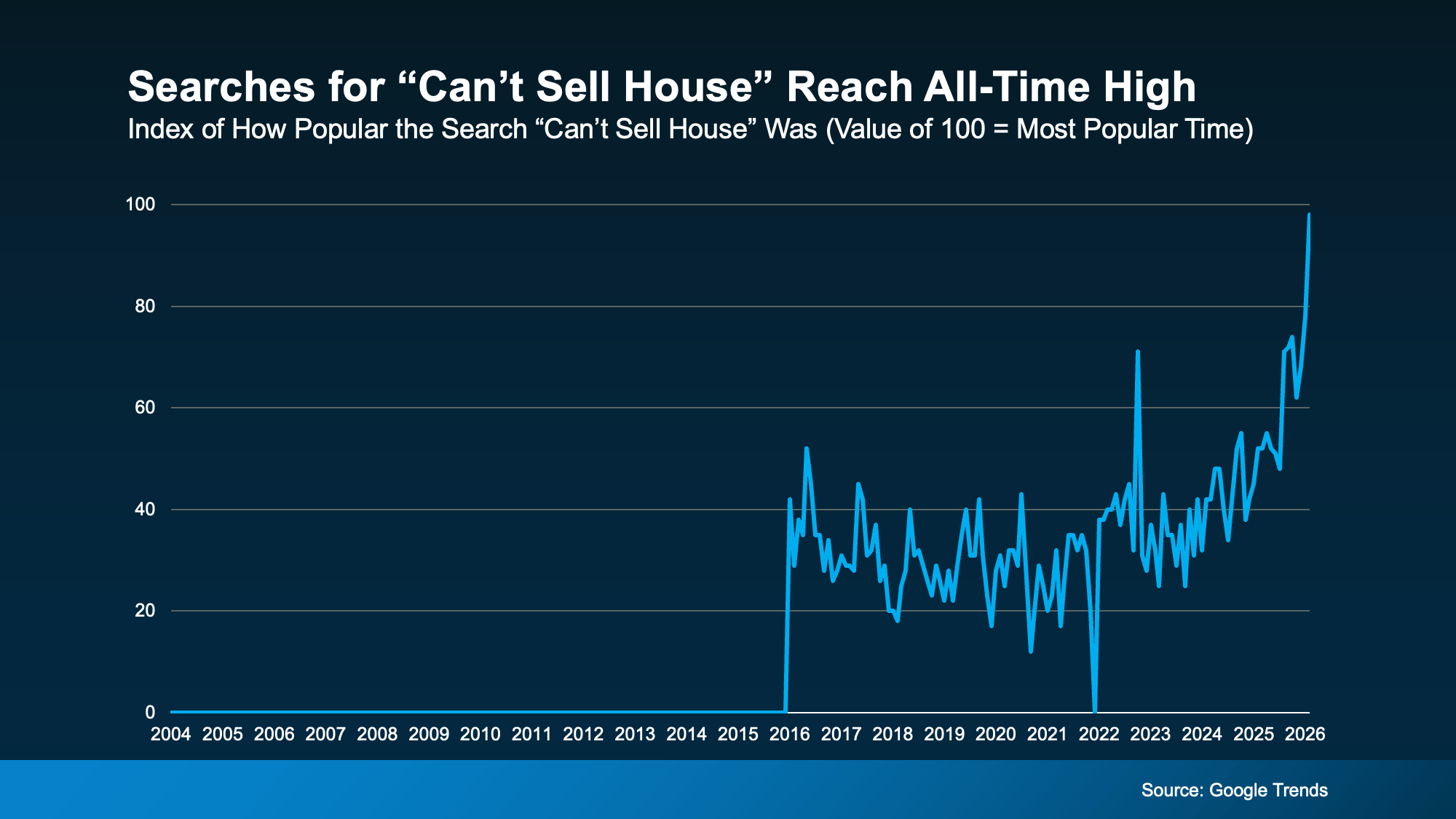

According to Zillow about 2.3% of homes available for rent were previously listed for sale. That may not sound like a lot, but it’s actually the highest share in almost 6 years.

Before you go that route yourself, it’s worth slowing down and looking at the full picture. Ask yourself these 3 questions first.

1. Would Your House Actually Work as a Rental?

What’s right for your situation is going to depend on your location, your home’s condition, and what the rental market looks like in your area. Think about:

- If you’re moving away, do you have a plan for how you’ll handle ongoing maintenance and repairs from afar?

- Does your house need repairs before it’s rental-ready? And do you have the time, energy, and the funds for that?

- What’s the market like in your area? Are there a lot of rental vacancies?

- What monthly rent could you realistically expect?

As C&C Property Management explains:

“At the heart of any rental market is the balance between supply and demand. When more tenants are looking for housing than there are available units, rental prices rise. On the other hand, if new construction adds hundreds of apartments or homes to a neighborhood, prices can soften as tenants have more choices.”

If your home would struggle to stand out or command the rent you need, that’s something to take seriously. Just because you can rent it doesn’t mean it’s the best option for you.

2. Are You Ready To Be a Landlord?

This is the part people don’t always think about upfront. On paper, renting sounds like easy passive income. But in reality, it’s a hands-on responsibility. Imagine:

- Taking midnight calls about clogged toilets or broken air conditioners

- Chasing down missed rent payments

- Covering unexpected repairs

- Fixing damage between tenants

And those costs can hit when you least expect them.

3. Have You Run the Real Numbers?

There’s also the financial side of things. For starters, renting out your house comes with extra expenses. Here are a few of the biggest according to Bankrate:

- Higher insurance premiums (landlord insurance typically costs about 25% more)

- Management fees (if you use a property manager, they typically charge around 10% of the rent)

- Routine maintenance and services

- Advertising fees to find tenants

- Gaps between tenants, where you cover the mortgage without rental income coming in

For some people, that’s totally manageable. For others, it’s more than they want to take on.

Your Next Step: A Conversation with Your Agent

Before you make any decision, talk to your current agent about overhauling your sales strategy first. Sometimes it’s not that buyers aren’t out there. It’s that something about the pricing, presentation, or marketing isn’t quite lining up with what they’re looking for.

And a few small adjustments can make a big difference.

Because while renting can be a great choice for the right person with the right house, if you’re only considering it because your listing didn’t get traction, there may be a better solution.

Bottom Line

If you’re torn between selling and renting, make sure to carefully weigh the pros and cons first. For some homeowners, the hassle (and the expense) of renting may not be worth it.

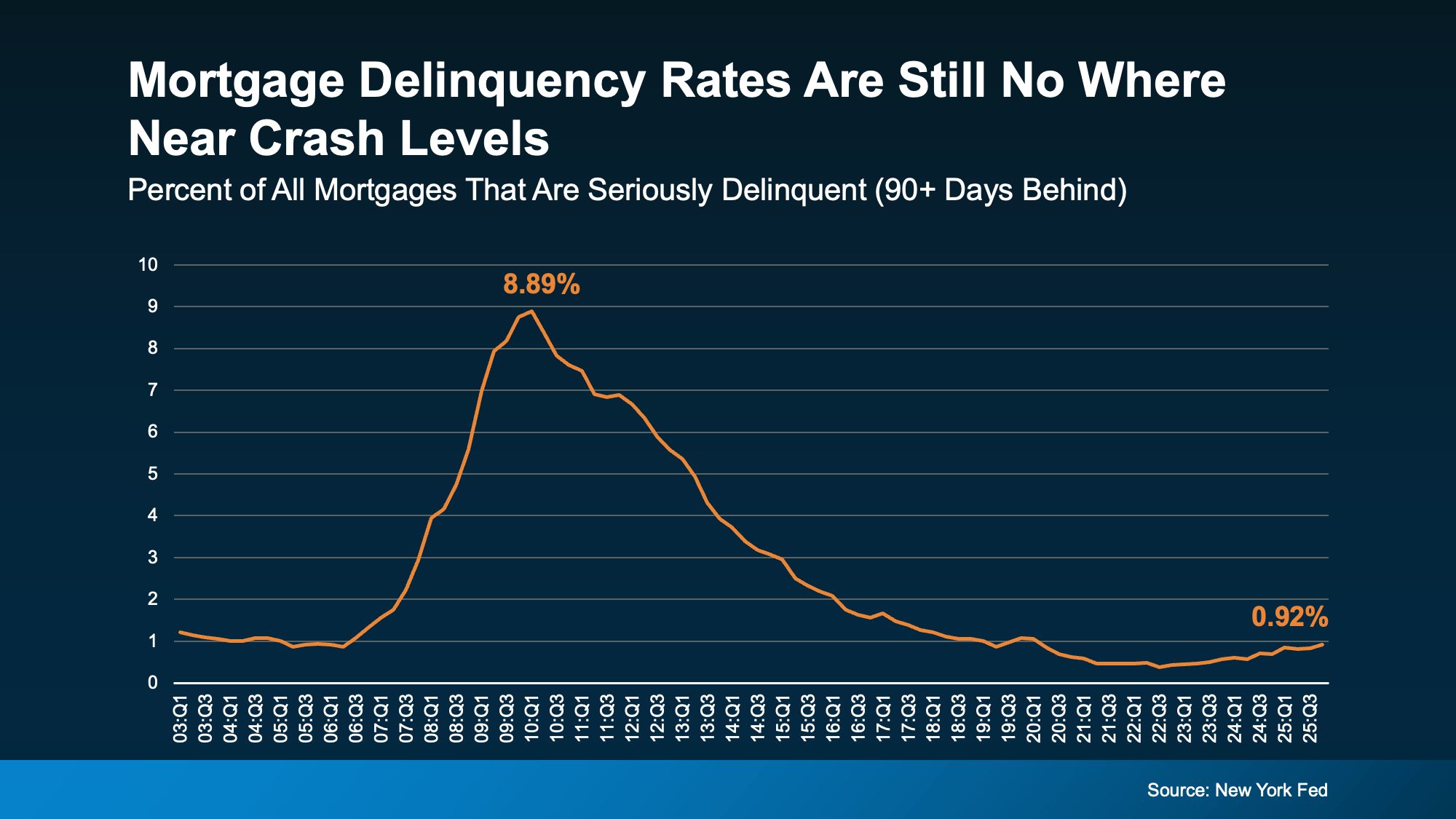

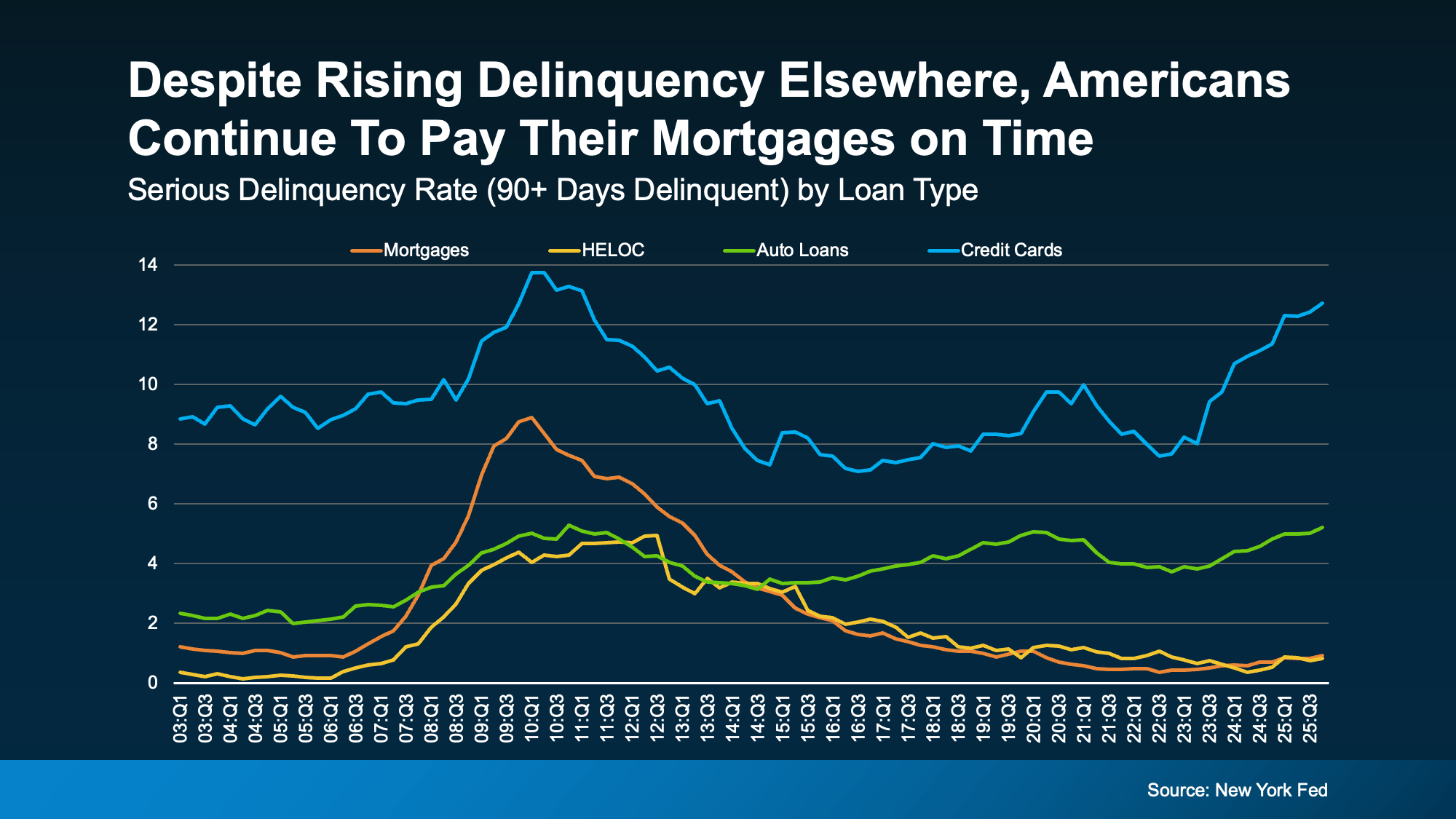

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.