Don’t Wait Until Spring To Sell Your House

As you think about the year ahead, one of your big goals may be moving. But, how do you know when to make your move? While spring is usually the peak homebuying season, you don’t actually need to wait until spring to sell. Here’s why.

1. Take Advantage of Lower Mortgage Rates

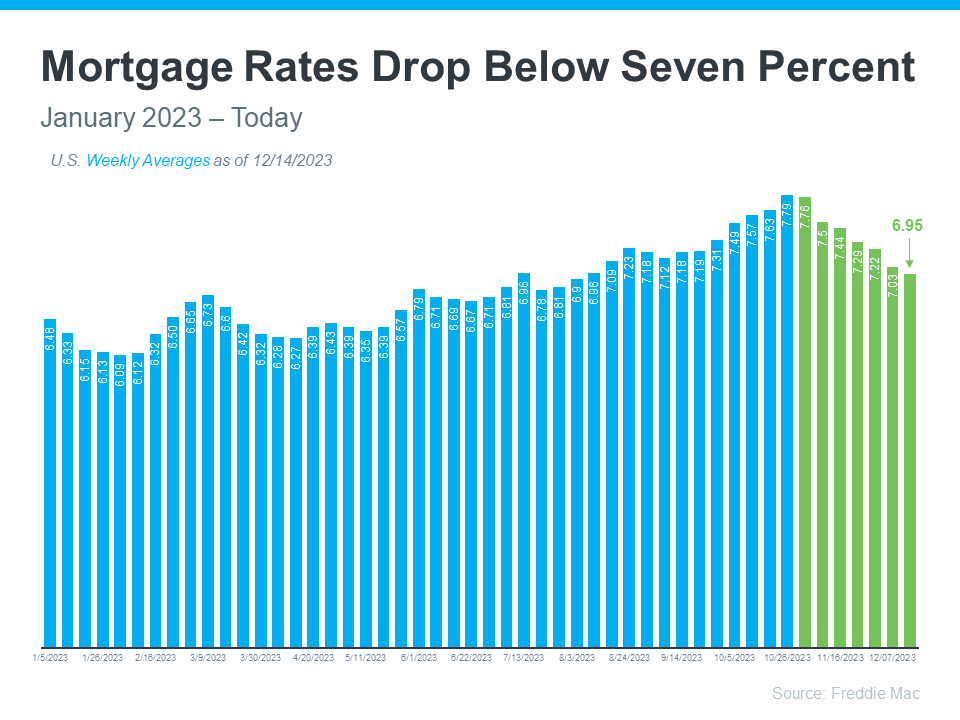

Last October, the 30-year fixed mortgage rates peaked at 7.79%. In January, they hit their lowest level since May. That means you may not feel as locked-in to your current mortgage rate right now. That downward trend in rates has made moving more affordable now than it was just a few months ago.

Another reason today’s rates make now a good time to sell? More buyers are jumping back into the market. Many had been waiting on the sidelines for rates to fall, but now that that’s happening, they’re eager and ready to buy. That means more demand for your house. According to Sam Khater, Chief Economist at Freddie Mac:

“Given this stabilization in rates, potential homebuyers with affordability concerns have jumped off the fence back into the market.”

2. Get Ahead of Your Competition

Right now, there are still more people looking to buy a home than there are houses for sale, which puts you in a great position. But keep in mind, with the recent uptick in new listings, we’re seeing more sellers may already be re-entering the market.

Listing your house now helps you beat your competition and makes sure your house will stand out. And if you work with an agent to price it right, it could sell fast and get multiple offers. U.S. News explains:

“When there is low housing inventory, sellers could get top dollar for their homes.”

3. Make the Most of Rising Home Prices

Experts forecast home prices will keep going up this year. What does that mean for you? If you’re ready to sell your current house and plan to buy another one, it may be a good idea to think about moving now before prices go up more. That would give you the chance to buy your next home before it gets more expensive.

4. Leverage Your Equity

Homeowners today have tremendous amounts of equity. In fact, a recent report from CoreLogic says the average homeowner with a mortgage has more than $300,000 in equity.

If you’ve been waiting to sell because you were worried about home affordability, know your equity can really help with your next move. It might even cover a big part, or maybe all, of the down payment for your next home.

Bottom Line

If you’re thinking about selling your house and moving to another one, connect with a local real estate agent to get the process started now so you can get a leg up on your competition.