14 Years Running: Why Real Estate Is Still America’s Favorite Investment

Quick gut reaction. Which investment do Americans trust more than stocks, gold, savings accounts, and bonds? The answer hasn’t changed in 14 years.

It’s real estate. And this year, that answer comes with even more conviction behind it. New data shows people aren’t just saying homeownership is a smart move, they’re feeling better about it than they have in years. Let’s dig into why.

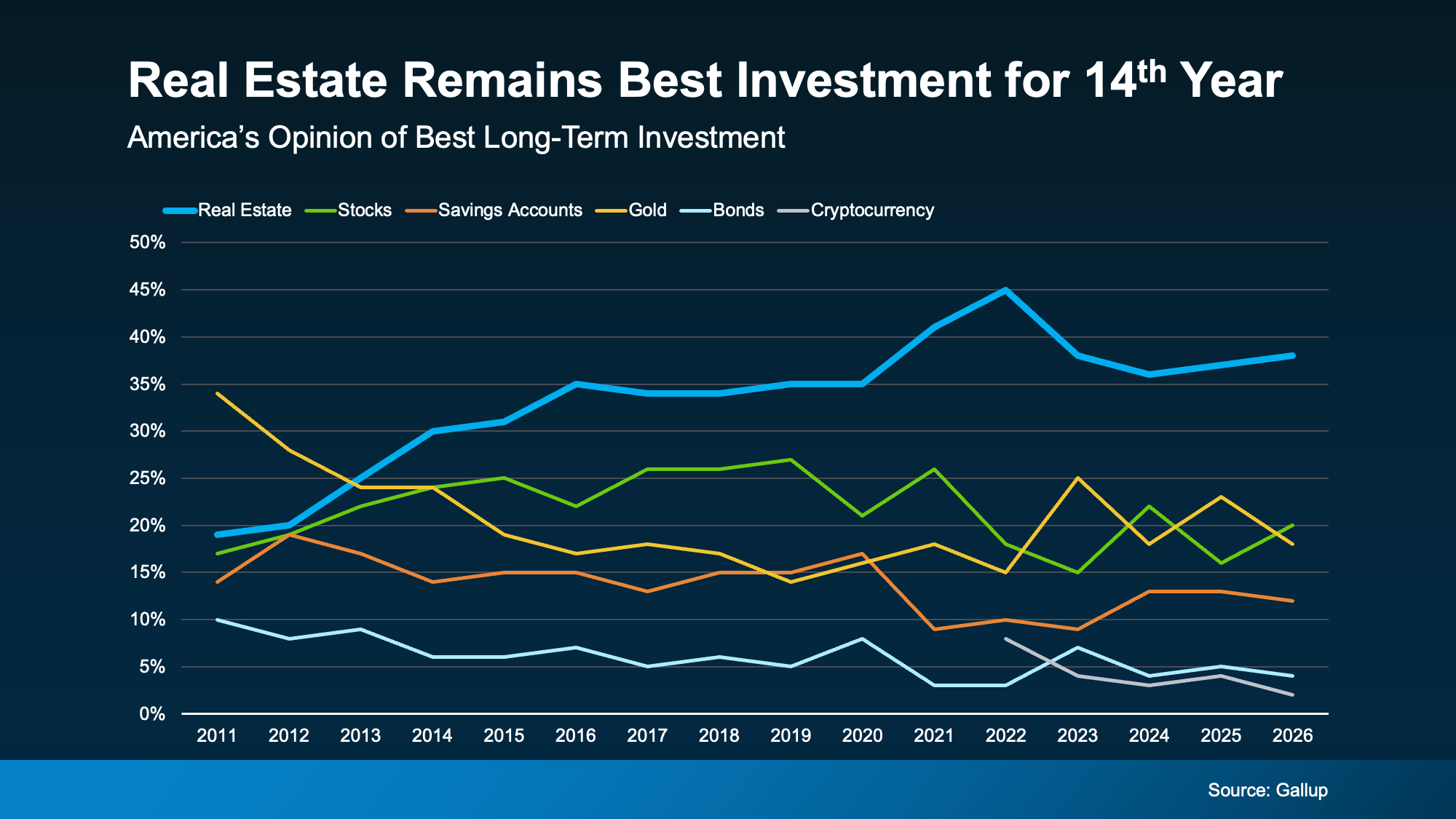

Real Estate Takes the Top Spot – Again

Every year, Gallup asks Americans to name the best long-term investment. And for the 14th year in a row, real estate came out on top (see graph below):

That’s not a fluke or a hot streak. That’s 14 straight years of beating out stocks, gold, and everything else.

Think about everything that’s happened in that stretch – rising rates, market swings, election years, you name it. Through all of it, Americans kept picking real estate. That kind of staying power says something about how people view homeownership – and it makes sense. Historically, it’s one of the best ways to build wealth in this country.

As Michelle Egan, Head of Credit Solutions, Impact Finance at JPMorgan Chase, explains:

“Owning a home has long been considered one of the most reliable ways to build wealth. Beyond providing shelter, a home is a valuable asset that can appreciate over time, build equity, and serve as a financial resource for generations.”

Now, you may have seen chatter online saying home prices are falling and wondered if that changes the math. It really shouldn’t. Nationally, home prices are still rising – just at a slower pace than a few years ago.

Yes, some local markets are seeing slight dips, but those dips are small compared to how much home values have grown over the past 5 years. Generally speaking, home prices almost always rise. As long as you plan to live there for a good length of time, you should still have the chance to build equity.

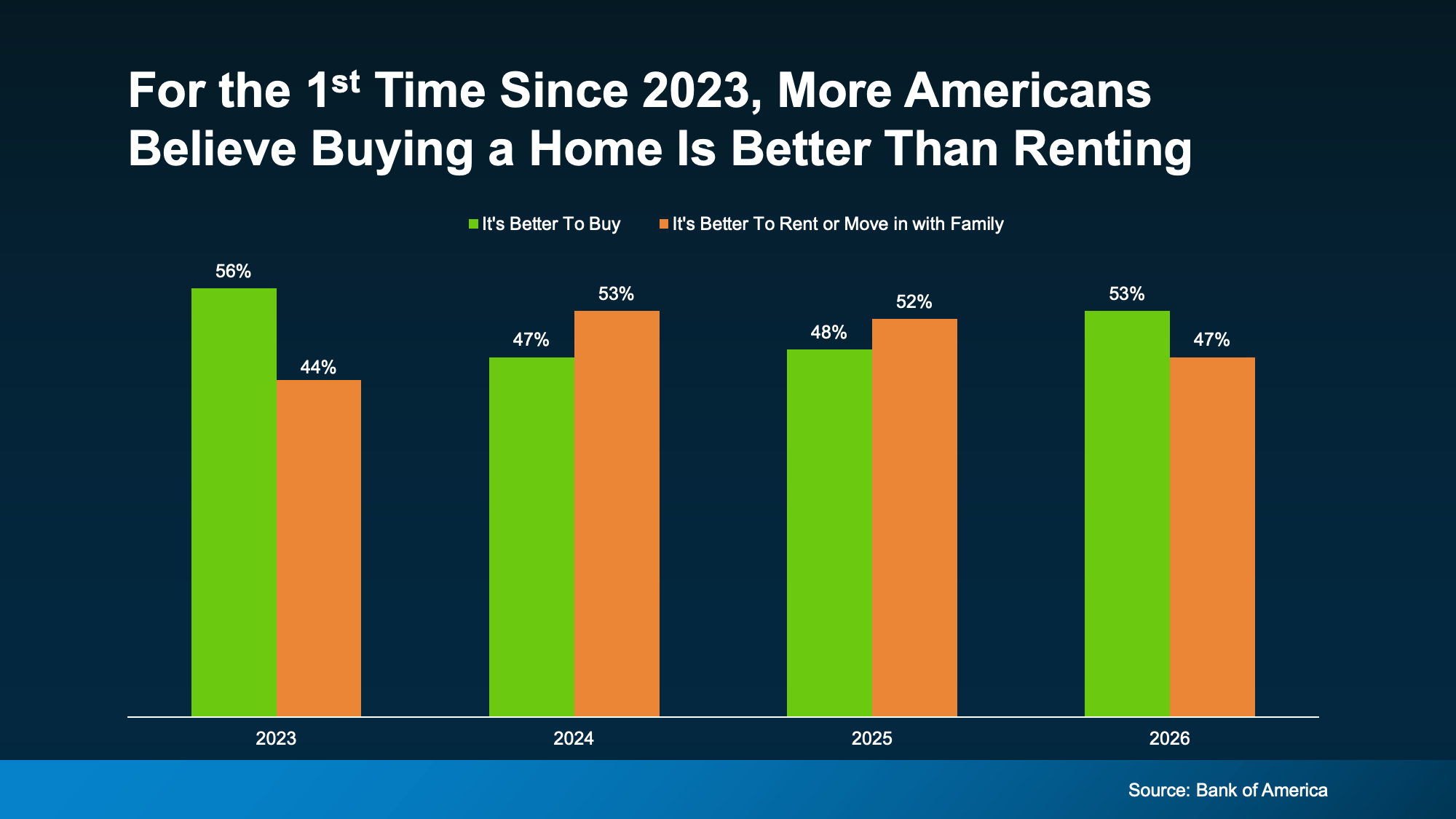

More People Say Buying Beats Renting

And while it’s true homeownership has been seen as a worthwhile pursuit for years now, something interesting is happening. It may actually be gaining a bit more popularity again.

According to Bank of America‘s latest Homebuyer Insights Report, 53% of people now say it’s better to buy a home than to rent or move in with family. That’s the first time buying has taken the lead since 2023 (see graph below):

In that same report, here are a few other signals that confidence in homeownership is on the rise:

-

90% of people say a home is a valuable investment, up from 79% just last year.

-

And 94% say owning a home provides stability, up from 83% the year prior.

Those are relatively big jumps in a short amount of time. And here’s what may be driving it.

It’s About More Than Money

Sure, affordability is still tight and some markets are still hard to break into, but that hasn’t changed what people feel about homeownership as a goal. And the reason why is simple – it’s not just a financial decision. It’s a lifestyle choice.

A home pays you back in ways stocks never could. As Sheharyar Bokhari, Principal Economist at Redfin, says:

“For many homeowners, a home is more than a place to sleep and store belongings—it’s a reflection of who they are. Homeownership can help people put down roots, build relationships and create a space that feels uniquely their own.”

You can’t get that from a brokerage account. A home is the one investment that grows your wealth and gives you a place to build your life. And that means something.

Bottom Line

For 14 years straight, Americans have called real estate the best long-term investment, and confidence in owning a home is on the rise. If you’ve been weighing whether buying is worth it, connect with a local real estate agent and talk through what that first step could look like for you.